")

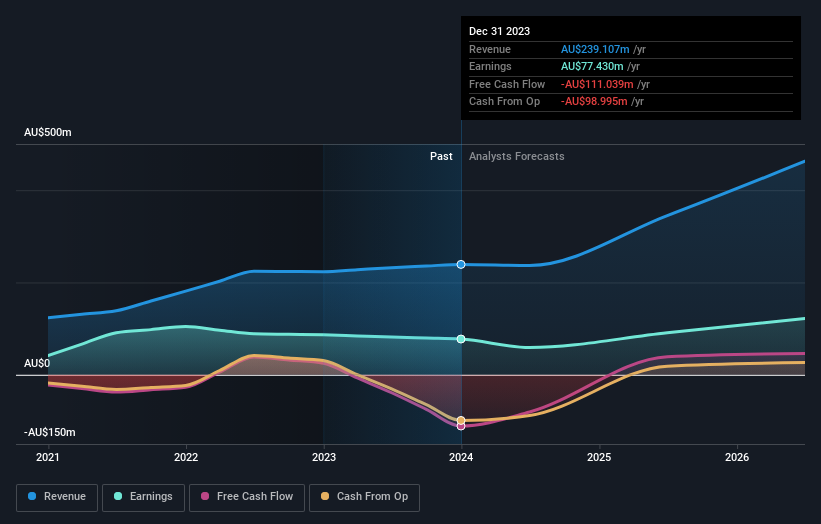

Analysts Covering LIFESTYLE COMMUNITIES LIMITED. (ASX:LIC) has today made significant revisions to its statutory forecasts for this year, resulting in negative news for shareholders. Revenue and earnings per share (EPS) estimates have both been revised downward, with analysts suggesting a significant deterioration in the business.

Following the downgrade, Lifestyle Communities' eight analysts now expect 2024 sales to be AU$237m, about the same as the previous 12 months. That's what it means. Statutory earnings per share for the period are expected to decline 11% to A$0.57. Before this latest update, analysts had been forecasting revenue of AU$268m and earnings per share (EPS) of AU$0.65 in 2024. Analyst sentiment has declined significantly, with revenue estimates having been revised down significantly and underlying earnings appearing to be lower. The same applies to per share figures.

Check out our latest analysis for Lifestyle Community.

The consensus price target fell 7.5% to A$16.29, with the weaker earnings outlook clearly driving analyst valuation expectations.

Looking at the bigger picture here, one way to understand these forecasts is to see how they compare to past performance and industry growth forecasts. These estimates suggest that sales are expected to slow and decline by 1.8% annually by the end of 2024. This represents a significant decrease from the 15% annual growth rate over the past five years. In contrast, our data shows that other companies in the same industry (covered by analysts) are forecast to see their revenue grow at 8.5% per year for now. Therefore, revenue is expected to shrink, but there are no bright spots for this cloud. The lifestyle community is expected to lag the broader industry.

conclusion

The biggest problem with the new estimates is that analysts have lowered their earnings per share estimates, suggesting business headwinds are ahead for the lifestyle community. Unfortunately, the company has also cut its revenue forecast, with its latest forecast suggesting that sales growth for the business will be slower than the broader market. Given the scope of the downgrade, it's no wonder the market has grown wary of the company.

As you can see, the analysts are clearly not bullish, but there may be a good reason for that. We identified several potential financial issues for lifestyle communities, including concerns about quality of earnings. For more information, click here to see this and the other 1 warning signs we've identified.

Another way to find interesting companies reach an inflection point It's about tracking whether management is buying or selling. free A list of growing companies that insiders are buying.

Have feedback on this article? Curious about its content? contact Please contact us directly. Alternatively, email our editorial team at Simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary using only unbiased methodologies, based on historical data and analyst forecasts, and articles are not intended to be financial advice. This is not a recommendation to buy or sell any stock, and does not take into account your objectives or financial situation. We aim to provide long-term, focused analysis based on fundamental data. Note that our analysis may not factor in the latest announcements or qualitative material from price-sensitive companies. Simply Wall St has no position in any stocks mentioned.