believes it has room to accelerate business growth")

Just because a company isn't making profits doesn't mean its stock price will go down. For example, if you've owned the stock since 2005, Salesforce.com, a software-as-a-service business, has lost money for years while its recurring revenue has grown, but if you've owned the stock since 2005, it's certainly a very It would have worked fine. Nevertheless, only a fool would ignore the risk of a loss-making company running out of cash quickly.

So the obvious question is, Zyme Works (NASDAQ:ZYME) shareholders are debating whether they should be concerned about its cash burn rate. In this article, we define cash burn as the amount of cash a company spends each year to fund growth (also known as negative free cash flow). First, we compare its cash burn to its cash reserves to calculate its cash runway.

Check out our latest analysis for Zymeworks.

When will Zymeworks run out of money?

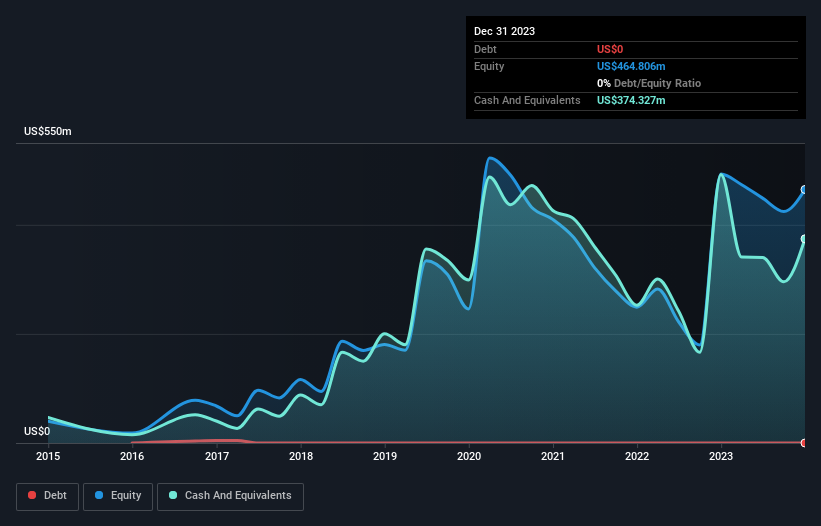

A company's cash runway is the amount of time it takes to use up its cash reserves at its current cash burn rate. As of December 2023, Zymeworks had cash of his US$374m and no debt. Looking at last year, the company burned through his US$122 million. In other words, it had a funding runway of approximately 3.1 years starting in December 2023. This length of runway gives the company the time and space it needs to develop its business. You can see how its cash balance has changed over time in the image below.

Is Zymeworks' revenue increasing?

Given that Zymeworks actually had positive free cash flow last year, we'll focus on operating revenue this year to get an idea of the trajectory of the business, before burning through cash. The bad news for shareholders is that operating revenue actually plummeted by 82% last year, which is of great concern in our view. However, it is clear that the key factor is whether the company will grow its business going forward. So it might be worth taking a peek at how much the company is expected to grow over the next few years.

Will Zymeworks easily raise more cash?

Given the declining revenue in question, Zymeworks shareholders will need to consider how they can fund growth if the company proves to need more cash. There is. The most common ways for publicly traded companies to raise more money for their operations is by issuing new shares or taking on debt. Many companies end up issuing new shares to fund future growth. By comparing a company's annual cash burn to its total market capitalization, we can roughly estimate how many shares it would need to issue to run the company for another year (at the same burn rate).

Zymeworks' cash burn of $122 million represents about 21% of its market cap of $583 million. This is not insignificant, and if the company had to sell enough shares to fund next year's growth at its current share price, it would likely witness significant and costly dilution. You'll probably end up doing it.

How risky is Zymeworks' cash burn situation?

In this analysis of Zymeworks' cash burn, we think its cash runway is reassuring, but we're a bit worried about its declining revenue. We're the kind of investors who are always a little concerned about the risks associated with cash-guzzling companies, but given the metrics we've discussed in this article, we feel relatively comfortable about the situation with Zymeworks. .A detailed investigation of the risks revealed 2 warning signs for Zymeworks Here's what readers should consider before investing money in this stock.

of course, You may find a great investment if you look elsewhere. So take a look at this free A list of companies that insiders are buying, as well as this list of growth stocks (based on analyst forecasts).

Have feedback on this article? Curious about its content? contact Please contact us directly. Alternatively, email our editorial team at Simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary using only unbiased methodologies, based on historical data and analyst forecasts, and articles are not intended to be financial advice. This is not a recommendation to buy or sell any stock, and does not take into account your objectives or financial situation. We aim to provide long-term, focused analysis based on fundamental data. Note that our analysis may not factor in the latest announcements or qualitative material from price-sensitive companies. Simply Wall St has no position in any stocks mentioned.