Chris Weeks/WireImage (via Getty Images)

It's often said that the best businesses are so simple that even an idiot can run them. Hanes Brands' innerwear business is one such business, and I think it is a business that has strong demand and operating income even in a recession. However, the value of the Hanes brand can be clouded by factors such as: The troubled activewear division appears to be shrinking and losing money at an alarming rate.

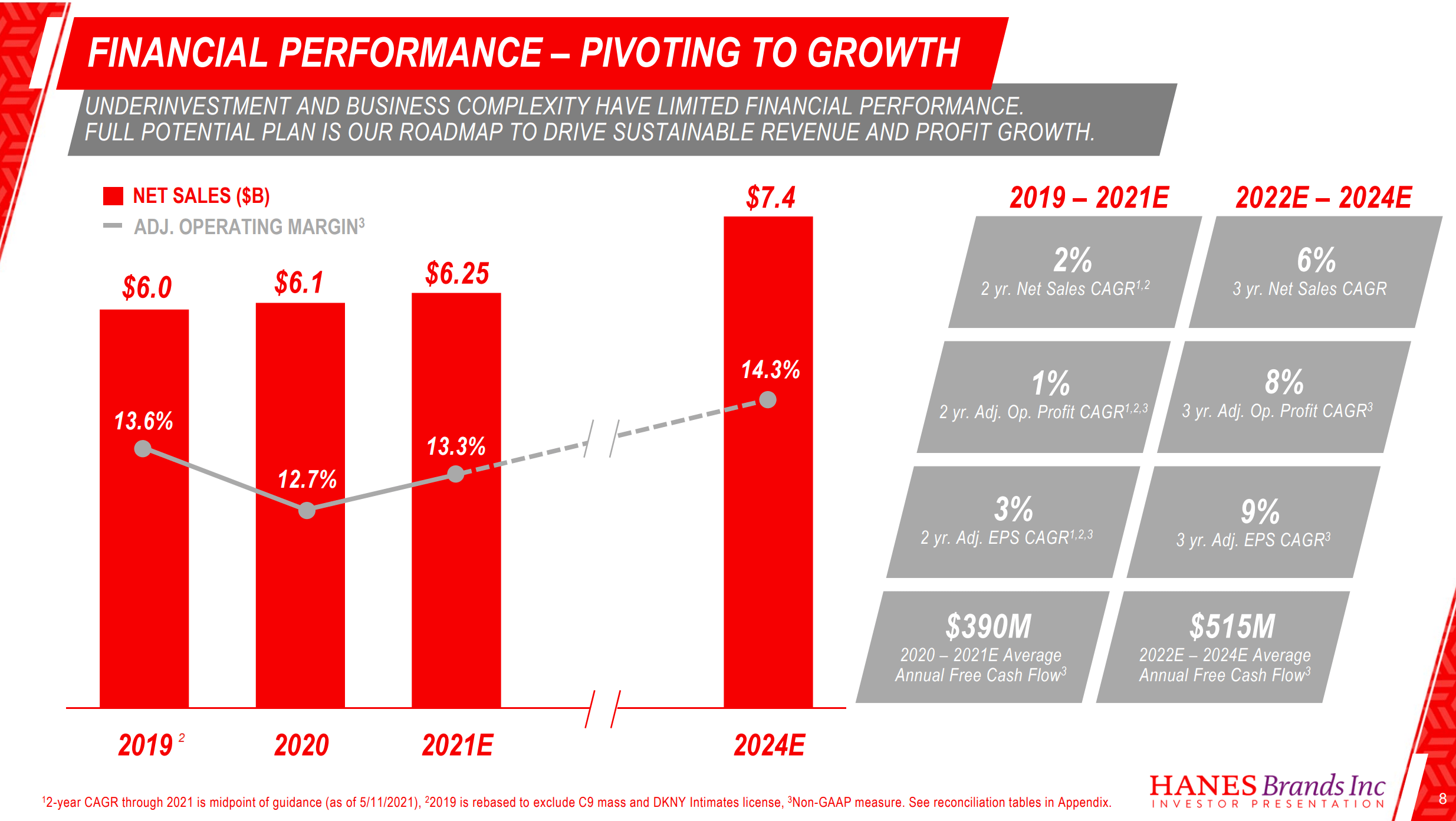

The last time I seriously looked into Hanesbrands Inc. was (New York Stock Exchange:HBIAt the time, I thought the company was in the middle of a three-year restructuring plan, but its early performance merited an F rating because sales were not on pace to meet its management plan of $7.4 billion by 2024. I commented. Operating margins are trending in the wrong direction (Figure 1).

Figure 1 – Hanes’ 2021 three-year restructuring plan (HBI investor presentation)

However, we recommended long-term Investors are looking to add to HBI stock because its valuation is “cheap” and Hanesbrands is paying an attractive dividend yield.

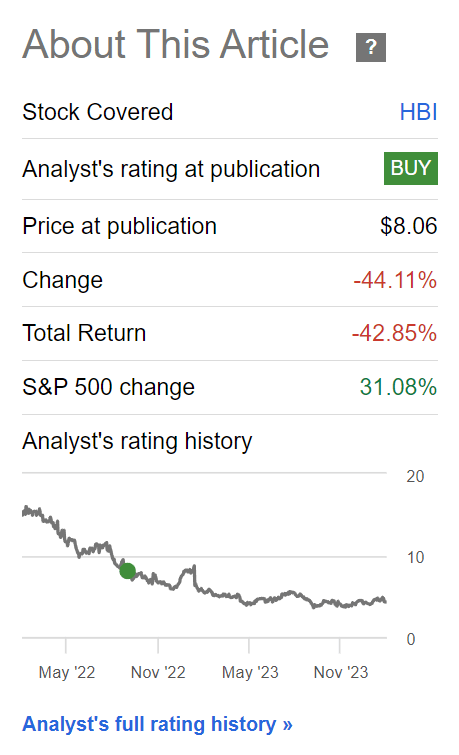

In retrospect, I wish they had withdrawn my recommendation. Since my article, HBI stock has fallen another 40%, for a total five-year return of -72% (Figure 2).

Figure 2 – HBI stock is down more than 40% since September 2022 (In search of alpha)

Due to a number of issues, Hanesbrands stock did poorly in 2023. First, Hanesbrands cut its dividend at the beginning of the year, and many investors who had bought the stock for a dividend yield of 7% or higher dumped the stock.

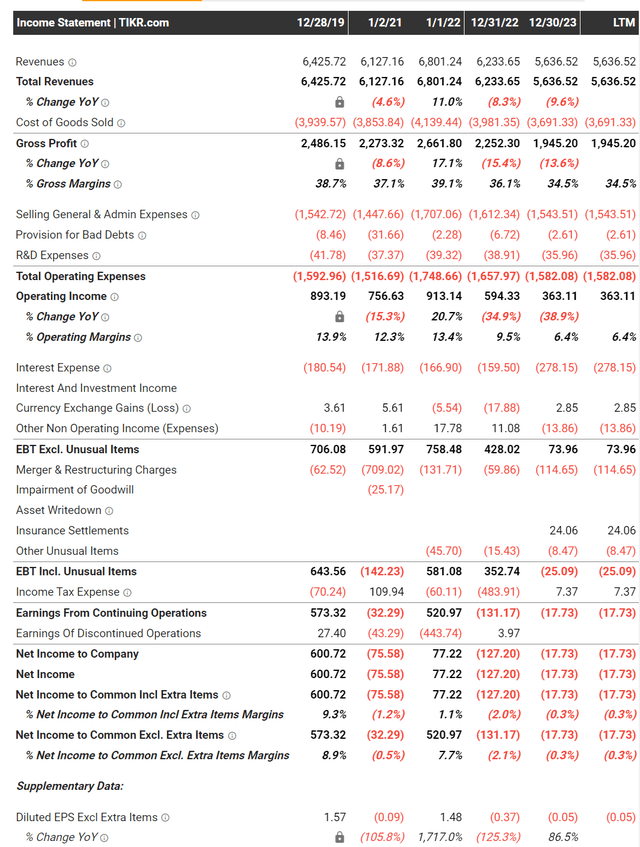

Furthermore, instead of reigniting the growth that management had planned, HBI's sales actually contracted, with full-year sales of just $5.6 billion in 2023 (down 7.6% year over year) and restructuring plans in 2021. The level was even lower than at the start (Figure 3).

Figure 3 – HBI Financial Overview (tikr.com)

Even more troubling for shareholders was that operating margins fell from 13.4% in 2021 to 9.5% in 2022 and just 6.4% in 2023.

Nothing to see in $1 billion in restructuring costs

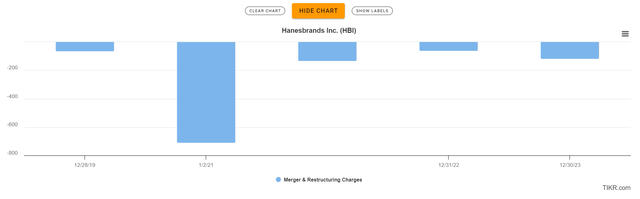

Overall, Hanesbrands has endured more than $1 billion in cumulative restructuring and M&A costs since 2019 (Figure 4). But the company is significantly weaker than when this whole restructuring ordeal began.

Figure 4 – Over $1 billion in wasted restructuring costs (tikr.com)

Champion's title stripped

The main cause of Hanes Brand's sales decline was Champion Brand, whose sales in the fourth quarter of 2023 were down 23% compared to the same period last year. Unfortunately, the brand's sales appear to be a closely guarded trade secret, as management has not provided financial numbers or tables for investors to track Champion's performance.

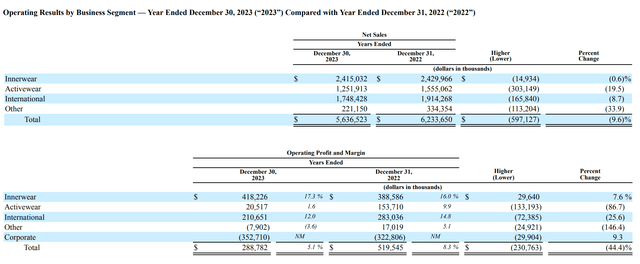

However, assuming the majority of activewear business segments are champions, sales in 2023 would be down 19.5% year over year to just $1.25 billion, with negative operating margins (Exhibit 5).

Figure 5 – HBI segmented performance (HBI 10K Report)

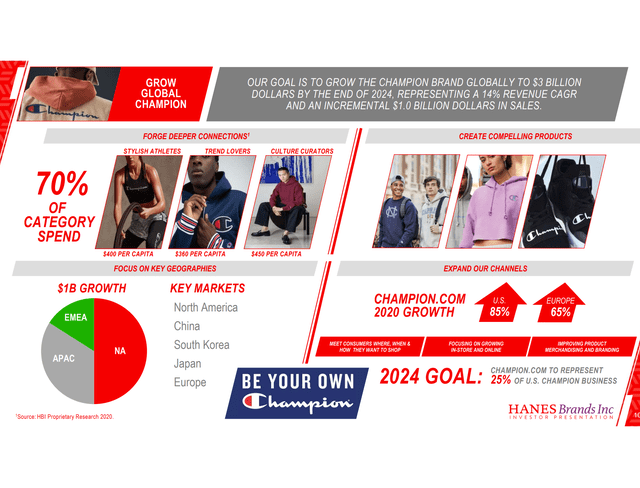

This is a marked departure from HBI's 2021 investor presentation, where management boasted that Champion would be a $3 billion brand by 2024 and a cornerstone of the company's overall growth strategy (Figure 6). .

Figure 6 – Management's plan was to grow Champion into a $3 billion business (HBI investor presentation)

Given this disappointing performance, HBI management has been publicly offering the Champion business since September 2023, and although the recent Q4 2023 earnings report did not provide details, it appears that a sale is imminent. No wonder it is said that there are.

However, all is not lost

However, I believe there is real value in the Hanes brand if management can sell Champion at the right price and reallocate the proceeds to reducing debt and refocusing on innerwear. .

First, referring to Figure 4 above, the innerwear business is a very stable and profitable cash cow. Despite the decline in top-line revenue, the innerwear division was able to generate sales of $2.4 billion in 2023 and operating margin was 17%. At its peak in 2020, the innerwear division had sales of $3 billion and an operating margin of 24%.

Selling underwear is essentially a fool-proof business, as consumers typically buy 8 to 10 sets (Berkshire Hathaway (BRK.A) (BRK.B) is Hanes Brand's main competitor). (which is likely the main reason for owning Fruit of the Loom). per year (Figure 7). As long as Hanesbrands doesn't screw up pricing or product mix, HBI will get its fair share of consumers' annual replenishment business.

Figure 7 – Innerwear is very stable (HBI investor presentation)

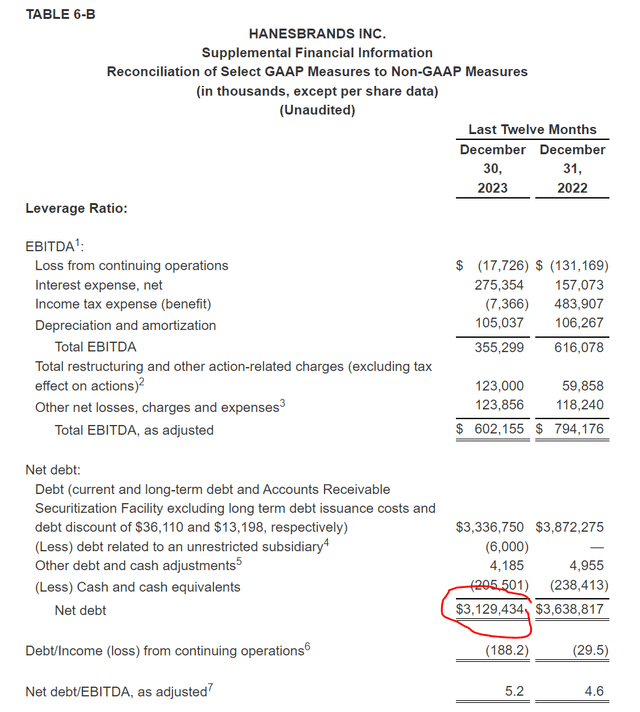

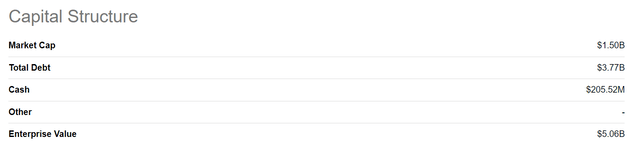

Assuming that Hanesbrands can generate a $1 billion profit for Champion, I believe it will go a long way toward reducing the company's high debt, which currently stands at $3.3 billion in total or $3.1 billion in net debt ( Figure 8).

Figure 8 – HBI is heavily in debt (HBI 10K Report)

Additionally, if the loss-making Champion business is abandoned, a leaner Hanesbrands could generate more free cash flow, which could be used to pay down more debt. In 2023, Hanesbrands generated free cash flow of his $518 million. This corresponds to a free cash flow yield of almost 10% on an enterprise value of $5.1 billion (Figure 9).

Figure 9 – HBI Corporate Value (In search of alpha)

The upside to valuation

In fact, if a company could generate the same level of free cash flow without a champion, each dollar of additional free cash flow would reduce net debt and increase equity value, assuming the company's value remains unchanged.

For example, if Hanesbrands can generate $300 million in FCF in 2024 (management is targeting $335 million), its net debt and leases could be reduced to $3.3 billion . Assuming the company value remains constant at $5.1 billion, the stock value increases by $1.8 billion, or 20%.

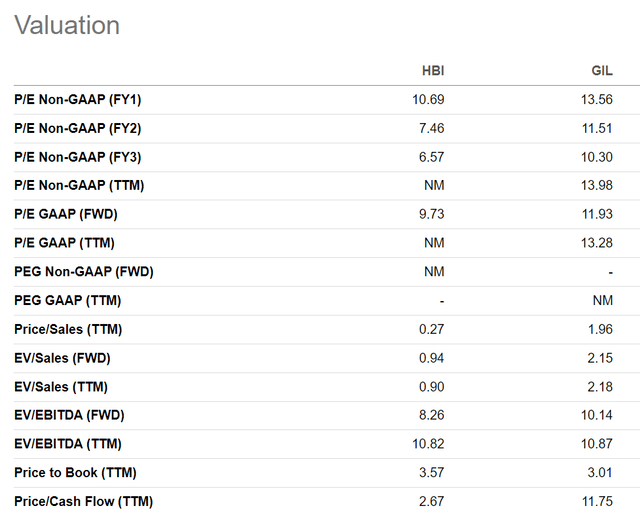

Perhaps if the company sells Champion and reduces its leverage, Hanes Brand's valuation could improve further, as many heavily indebted companies are penalized for their debt weight. For example, HBI trades at a multiple of 8.3x forward EV/EBITDA, while Gildan Activewear (GIL), a Hanes brand competitor with a much better balance sheet, trades at 10.1x forward EV/EBITDA (Figure 10) .

Figure 10 – HBI vs. GIL (In search of alpha)

Risks to Hanesbrands

The biggest risk for Hanes Brands is that if Champion doesn't sell and the company continues to shrink, its activewear division's operating losses could start to snowball quickly. Additionally, management's attention may be diverted from our core innerwear business and we may lose market share to competitors.

On the other hand, if Hanesbrands were able to sell Champion for a higher-than-expected price, it would clearly be able to deleverage more quickly and reallocate capital to resume growth in its core innerwear business.

conclusion

I believe Hanesbrands' 2021 turnaround plan has been a complete failure so far, with sales and operating margins far below where they were at the start of the turnaround plan.

But despite disappointing results, Hanesbrands has a valuable “solid” innerwear business.

Based on management's guidance of approximately $300 million in 2024 FCF, I believe Hanesbrands stock should rise more than 20% if the company can apply that to deleveraging. If the company can offload its struggling Champion business for a fair price, it could accelerate debt reduction and create more shareholder value.I rate HBI stock a. speculative buying For contrarian investors.