believes it needs to carefully drive business growth")

Even when a company is making a loss, it is possible for shareholders to make a profit if they buy a good company at an appropriate price. For example, if you've owned the stock since 2005, Salesforce.com, a software-as-a-service business, has lost money for years while its recurring revenue has grown, but if you've owned the stock since 2005, it's certainly a very It would have worked fine. That being said, there are risks involved, as unprofitable companies can burn through all their cash and go into distress.

So the obvious question is, bioatla (NASDAQ:BCAB) shareholders are debating whether they should be concerned about its cash burn rate. In this article, we define cash burn as the amount of cash a company spends each year to fund growth (also known as negative free cash flow). The first step is to compare its cash burn to its cash reserves to uncover its 'cash runway'.

See our latest analysis for BioAtla.

When will BioAtla's funding run out?

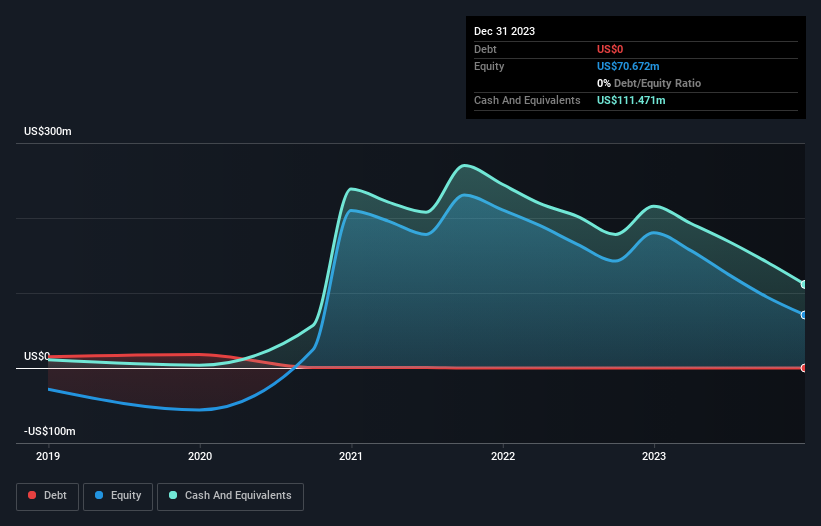

A company's cash runway can be calculated by dividing the amount of cash it holds by the rate at which it spends that cash. As of December 2023, BioAtla had cash of US$111 million and no debt. Looking at last year, the company burned through his US$104 million. So it had a cash runway of about 13 months starting in December 2023. This isn't too bad, but unless cash burn significantly reduces, it's safe to say that the end of the cash runway is in sight. The image below shows how its cash balance has changed over the past few years.

How has BioAtla's cash burn changed over time?

BioAtla did not record any revenue last year, which indicates that the company is still an early-stage company developing its business. Nevertheless, we can examine its cash burn trajectory as part of assessing its cash burn situation. The company's cash burn actually increased by 15% in the last year. This suggests that management is ramping up investment for future growth, but not very quickly. However, if spending continues to rise, the company's actual cash runway will be shorter than implied above. However, it is clear that the key factor is whether the company will grow its business going forward. For this reason, it makes a lot of sense to see what analysts are predicting for the company.

How easily can BioAtla raise funding?

BioAtla has a solid cash runway, but its cash burn trajectory may have some shareholders thinking ahead to when the company may need to raise more cash. Companies can raise capital through debt or equity. One of the main advantages of publicly traded companies is that they can sell stock to investors to raise cash and fund growth. By looking at a company's cash burn compared to its market capitalization, insight into how much shareholders will be diluted if the company needs to raise enough cash to cover another year's cash burn. It can be obtained.

BioAtla has a market capitalization of US$166 million, and last year it burned through US$104 million, or 63% of its market value. This suggests that the company's expenses are very high relative to its size, making it a very risky stock.

So should we be worried about BioAtla's cash burn?

In this analysis of BioAtla's cash burn, we think its cash runway is reassuring, but we're a little worried about its cash burn relative to its market capitalization. After considering this range of actions, we think shareholders should pay close attention to how the company uses its cash, as its cash burn makes us uncomfortable.On a different note, BioAtla has 3 warning signs (and two that can't be ignored) that I think you should know about.

of course BioAtla may not be the best stock to buy.So you might want to see this free A collection of companies with a high return on equity, or a list of stocks that insiders are buying.

Have feedback on this article? Curious about its content? contact Please contact us directly. Alternatively, email our editorial team at Simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts using only unbiased methodologies, and articles are not intended to be financial advice. This is not a recommendation to buy or sell any stock, and does not take into account your objectives or financial situation. We aim to provide long-term, focused analysis based on fundamental data. Note that our analysis may not factor in the latest announcements or qualitative material from price-sensitive companies. Simply Wall St has no position in any stocks mentioned.