")

spxChrome

Big 5 Sporting Goods (NASDAQ:BGFV) is another legacy brick-and-mortar retailer whose stock has a seen trouble in recent times.

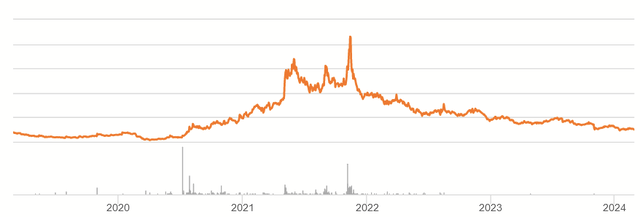

5Y Stock Price (Seeking Alpha)

2022 and 2023 were spent in gradual decline. Yet, there may be opportunity in this decreased valuation, so I’m going to give an overview of how the business has been doing over the years, discuss recently released results for FY 2023, and explain why I think BGFV stock is a SELL.

Company History

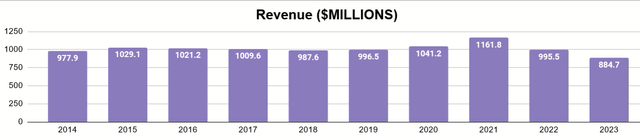

Founded in 1955, the company gets its name from its first five stores that opened in California and its specialty in sporting goods. Ownership changed hands a few times in the following decades, and the company didn’t go public until 2002. Below, I’ll show some key financial data of the company from the past ten years.

Author’s display of reported data

Revenues remained largely flat for most of the decade, ultimately hitting a low of $864.7M in 2023. One basic explanation for this is their size by store count hasn’t changed much in this time.

2018 and 2023 Forms 10K

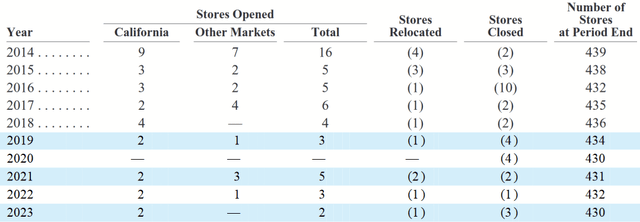

In their Q4 2023 financial results, they announced that they have 430 stores currently. Store count somewhat tracks the fluctuations in revenues, but clearly there is more to it than that, as they increased in 2020 and 2021. What was the cause of this? As management explains (2020 Annual Report, pg. 29):

Our same store sales increased 3.0% for fiscal 2020 versus the comparable 53-week period in the prior year. Same store sales in fiscal 2020 increased for our major merchandise category of hard goods, and decreased for our footwear and apparel categories, and primarily reflected strong consumer demand for various products as a result of the COVID-19 pandemic for most of the fiscal year.

You might be wondering how a brick-and-mortar operation benefited from COVID (when virtually all of them suffered), but you might also remember a fad that formed as a response to the quarantining and social distancing: camping for vacation. Big 5 wasn’t the only business to see increased sales from this. A comparable example was in Thor Industries (THO), which sells RVs and also saw a spike in revenues from this adjustment.

Thor’s Revenues (Seeking Alpha)

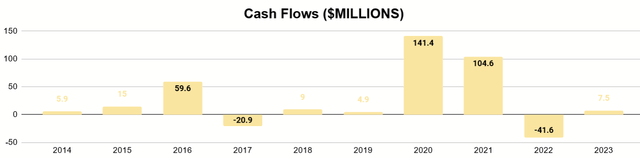

Since retailers tend to operate with tight margins (Big 5 being no exception), this spike in sales increased their free cash flow quite a bit. Below is the decade-long history to illustrate it.

Author’s display of 10K data

With capex rarely above $20M (and this was earlier in the decade when more stores were being added), revenue fluctuations are one of the biggest influences on a year’s FCF. What did the company ultimately choose to do with this cash?

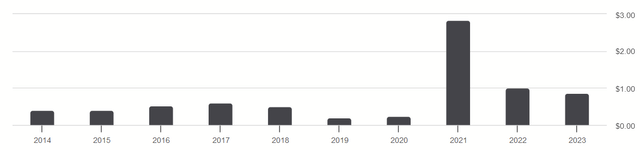

BGFV Dividends Per Share (Seeking Alpha)

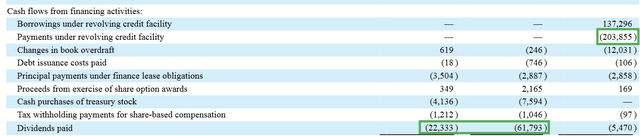

Why, it used it to pay out bigger dividends to shareholders. $61.8M in cash dividends were paid to shareholders for 2021. On top of that, they completely wiped out their long-term debt.

2022 Cash Flow Statement

Yet, this windfall of cash was not to last. In their Q4 2023 conference call, CEO Steven Miller reported:

Our fourth quarter results were disappointing, as our top line was impacted by ongoing macroeconomic challenges, pressuring consumer discretionary spending, coupled with extraordinarily unfavorable winter weather conditions across our Western footprint.

Net sales for the fourth quarter were $196.3 million compared to $238.3 million in the prior year, reflecting a 17.7% decrease in same-store sales. Winter-related products are typically an important seasonal driver of our fourth quarter business. But this year’s warm weather and lack of snow weighed heavily on the category’s performance, which was down nearly 40% versus the prior year.

The benefits of COVID not only expired, but an increased inflationary environment also reduced sales, leading to a dividend reduction at $0.05 per quarter.

Business Model and Strategy

As of 2023, the company has 430 stores in 11 U.S. states. In their many annual reports, you’ll find the following language about their business strategy (2023 Form 10K, pg. 5):

Throughout our operating history, we have sought to expand our business with the addition of new stores through a disciplined strategy of controlled growth. Our expansion within the western United States has typically been systematic and designed to capitalize on our brand recognition, economical store format and economies of scale related to distribution.

This largely explains why store count has remained flat. Big 5 hasn’t been rushing to grow or to penetrate markets where it isn’t sure that it will be successful. They also note what they believe to be advantages from their store model:

Our store format enables us to have substantial flexibility regarding new store locations. We have successfully operated stores in major metropolitan areas and in areas with as few as 30,000 people. Our 12,000 average square foot store format differentiates us from superstores that typically average over 35,000 square feet, require larger target markets, are more expensive to operate and require higher net sales per store for profitability.

big5sportinggoods.com

Merchandise includes a wide variety of sporting/outdoor equipment and apparel, featuring many well-known brands, along with some of their own private labels. They break this down into “soft goods,” such as shirts and shows and “hard goods,” which includes tougher, bulkier items like baseball gloves and exercise equipment.

2023 Form 10K

While there is some variability, these make up a fairly even portion of their sales.

big5sportinggoods.com

The company has an e-commerce platform on their website in addition to the brick-and-mortar operation. From what I can tell, they do not break down their online sales from that of the physical stores, so this contribution to their bottom line is unclear.

Distribution Center (phelandevelopmentcompany.com)

They utilize a single distribution center in Riverside, CA to deploy their inventory to all of their stores.

Seeking Alpha

Earlier I said Big 5 used their cash to wipe out their long-term debt, but I should add clarity. Most of that debt came from tapping into their credit facility, which would make sense to do at the onset of COVID. Realistically, the company has never been heavily leveraged, and given the lack of growth, it’s not had much reason to change that.

Dividends and Buybacks (Seeking Alpha)

As the rest of their capital allocation goes, usually most of FCF is paid out as dividends, with between a third and a fourth as much being used for buybacks.

A Look to the Future

While the business is financially healthy and otherwise stable, it’s important to take a nuanced look at things and weigh the risks with the positives. I’ll start by highlighting my main concern.

Competition

Retail is infamously competitive, forcing stores to keep prices low and endure narrow operating margins. Looking at the flat store count over the decade, I believe this to be a sign that management consistently sees expansion as a risk to their bottom line, as opposed to a benefit. A failed store is lost capital.

Risk Factor: Competition (2023 Form 10K)

Above, I’ve screenshot one of their risk factors from their 10K. There, they listed various retailers with whom they compete (and I’m grateful they do this because most companies are hesitant to name their competition in their 10K). Among those, you’ll see some other brands that have been struggling or suffering long-term decline: Foot Locker (FL), Kohl’s (KSS), and JCPenney (JCP before it filed for bankruptcy and got acquired).

You’ll also see some giants there that haven’t struggled to make money over the last decade: Amazon (AMZN), Walmart (WMT), and Target (TGT). When I look at Big 5, I can’t see what kind of advantage it is supposed to have that stands the test of time against them. I live in the east cost where there are not Big 5 stores, but when I needed a camping chair, I went to Walmart; I didn’t go to a Dick Sporting Goods or another chain with a sporting focus. I went to the big boys. I don’t think I’m unusual in that regard, either.

Of course, I’m looking really hard at businesses like Amazon when it comes to this concern.

E-Commerce

The future of e-commerce plays a very important role in this competitive landscape. I want to bring up this interesting data point. Total e-commerce sales in the U.S. accelerated under COVID but did not return to pre-COVID levels.

U.S. E-Commerce Sales (marketplacepulse.com)

That spike you see is a quarter-over-quarter leap of $50 billion in sales, and it did not revert. Big 5’s sales not only reverted; they are the lowest they’ve been in a decade. While Big 5 hasn’t broken down its online sales in its latest 10K from store sales, I can’t help but feel that it would show a disappointing number, based on these trends.

I try to look at this from a customer mindset. Most people are in the habit of doing an online purchase primarily from Amazon by now. If they want sporting goods, they can find just about any brand and price range on Amazon. They also know that Amazon’s delivery is on-point, which is a big part of the draw. Sporting goods can often be large and unpleasant to lug around, so the temptation to have it shipped instead of driving to get it yourself is higher than ever.

I don’t see Big 5’s future in this space. Where is management’s focus? Let’s quote the earnings call again:

In the face of a challenging sales environment, we have continued to focus on the aspects of the business that we have more control over, such as merchandise margins, inventory levels and expense management.

This is a good mindset; make no mistake. You’d be surprised how many managers can forget the basics like that. Yet, their online platform comes off as more of a formality, and I suspect their only real hook is with local customers who are likely familiar with store brand and perhaps really like their nearby store.

Dividends and Buybacks

Without an obvious path for growth, the main hope for long-term value accumulation is going to be buybacks at prices that provide a similar return on capital as growth would and heavy dividend distributions. Thankfully, management paid dividends while the going was good and didn’t blow the cash flow from 2020 and 2021.

Yet, given the recent dividend cut that annualizes to $0.20 per share and their vulnerability to macro-factors like inflation, anybody interested in taking a long-term position would need to think critically about whether or not to reinvest these dividends at the time of their payment. Moreover, I can’t see BGFV having the consistent cash flow needed for anyone that might see the dividend as an income source.

Valuation

We now come to the valuation. As usual, I prefer to use a Discounted Cash Flow model. Since the business is not growing and does not expect to grow, I won’t calculate that. As such, it’s mainly a matter of what I estimate typical free cash flow to be, and it pays to be very cautious on that figure since there is no perceivable growth.

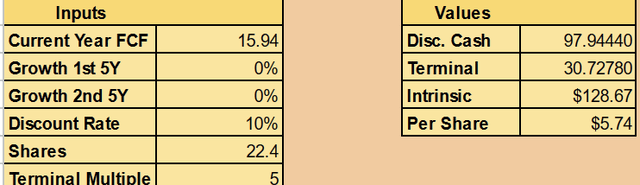

If we average the last decade of FCF, that gives $28.54M per year. Yet, that figure is troubled because so much of that average was pulled up by 2020 and 2021. I’m not trying to deny Big 5 fair credit, but COVID was a very bizarre event (perhaps once in a century), and I don’t imagine that we can count on it to replicate itself for a cash flow analysis going forward. If we cap what we count from those years at $60M (since that was the high point of $2016), we get a more conservative and realistic average of $15.94M. Let’s run the numbers.

Author’s calculation

Using a Terminal Multiple of 5 (again, no reason to expect a non-grower will trade at a premium down the road), that gives an intrinsic value of $128.7B for the market cap and thus $5.74 per share. Additionally, folks may consider that with no debt and $9.2M in cash, that resolves to about $0.41 per share in net cash.

As I write this, the share price has fallen in response to the Q4 news, to a $115M market cap and less than $5 per share. You might say, “It’s undervalued; it’s a buy.” I won’t say that, and instead I will say that it’s a Sell.

The reason is simple. While the business has been mostly stable over the past decade, its recent results show that it’s not an industry leader, and while it hasn’t suffered the same setbacks as other legacy retailers, it still seems vulnerable to disruption to come.

Moreover, lacking growth, investors should demand a much greater margin of safety than what the current price suggests. Personally, I’d want less than $3 per share with the same fundamentals before I even started to think about it. You can make money by buying a great, thriving company at a modest discount, but that’s not the offer you get with Big 5.

Conclusion

Big 5 Sporting Goods is a well-run vendor of sporting goods in the Western U.S. It’s avoided financial troubles that many other retailers have encountered over the past decade, but it also has only managed to tread water, and management gives a fairly frank outlook that that will continue to be the case, with potential buybacks and dividends being the saving grace for this investment.

One can mathematically argue that the company is undervalued, but the problem with such a business is that it can’t keep up, and this makes it easy for investors to get strung along for years by a stock price that seems alluring. While I don’t believe BGFV will go to zero, they will likely get mediocre returns, and there’s no obvious exit plan for such an investment. Until there is a much steeper discount or at least a better dividend yield, I don’t think it’s a buy or a hold. I think it’s a common sense SELL.