Paychex Inc. (NASDAQ:PAYX) stock is up about 196% over the past decade, delivering a decent annual compound return of 11.60% for long-term investors. The company also pays dividends continuously without interruption every year. Based on my analysis, this business services company appears to have a fairly good valuation right now.

Expand profits with high sustainable operating margins

Paychex helps more than 740,000 small and medium-sized businesses around the world with payroll, benefits, and insurance as part of a holistic human capital management solution. The company's software-as-a-service (SaaS) product, his Paychex Flex platform, provides customers with a total employee management solution from recruiting to hiring to termination.

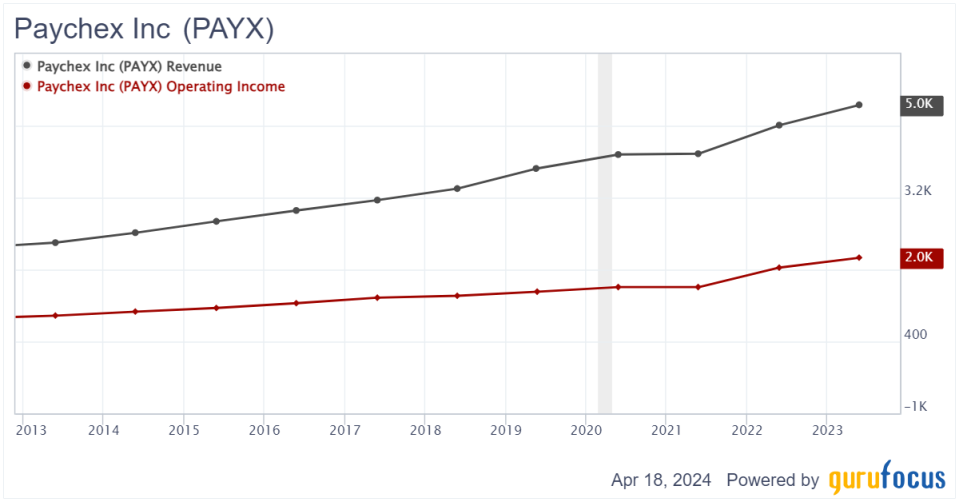

The company has seen significant revenue growth over the past decade, jumping from $2.33 billion in 2013 to $5 billion in 2023. At the same time, operating profit also reflected this upward trend, increasing from $905 million to $2 billion.

PAYX Data by GuruFocus

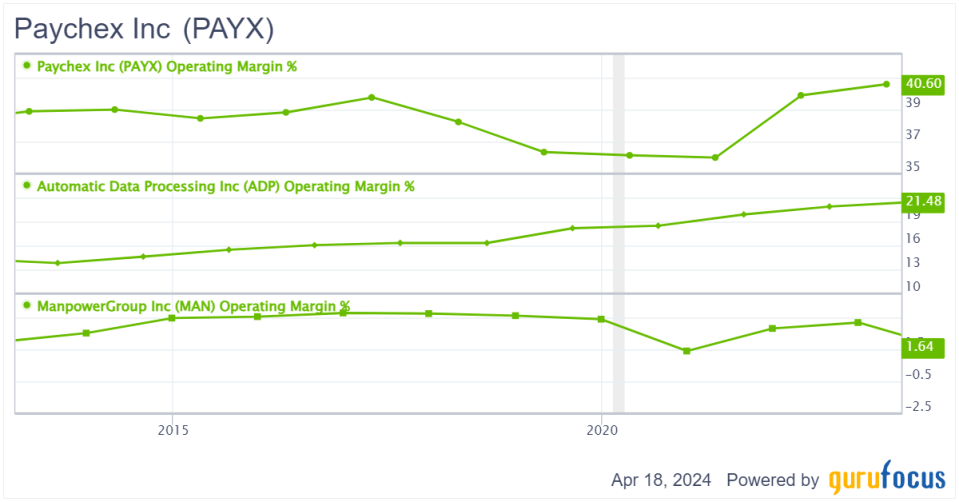

Paychex's business model is highly profitable, featuring high operating margins ranging from 36% to 40.60%. Consistently high operating margins demonstrate that the company efficiently manages operating costs under a variety of economic conditions, resulting in strong and sustainable profitability.

Compared to peers such as Automatic Data Processing (NASDAQ:ADP) and ManpowerGroup (NYSE:MAN), Paychex has much better operating margins. His operating profit margin in 2023 remains at 40.60%, almost double Automatic Data Processing's operating profit margin of 21.50%. On the other hand, ManpowerGroup's operating margin was a very low 1.64%.

PAYX Data by GuruFocus

Improving return on invested capital

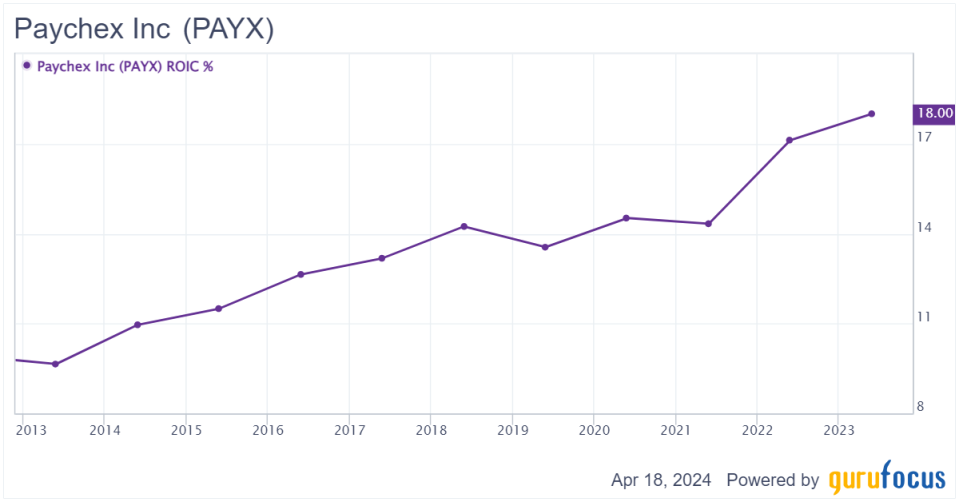

Another impressive factor is the company's consistently improving return on invested capital. His ROIC for the company nearly doubled from 9.65% in 2013 to 18% in 2023. His consistent increase in ROIC over the past 10 years shows that the company can grow its customer base, revenue, and profitability without proportionately increasing investments in infrastructure, systems, and operations. .

PAYX Data by GuruFocus

Generate consistently positive cash flow

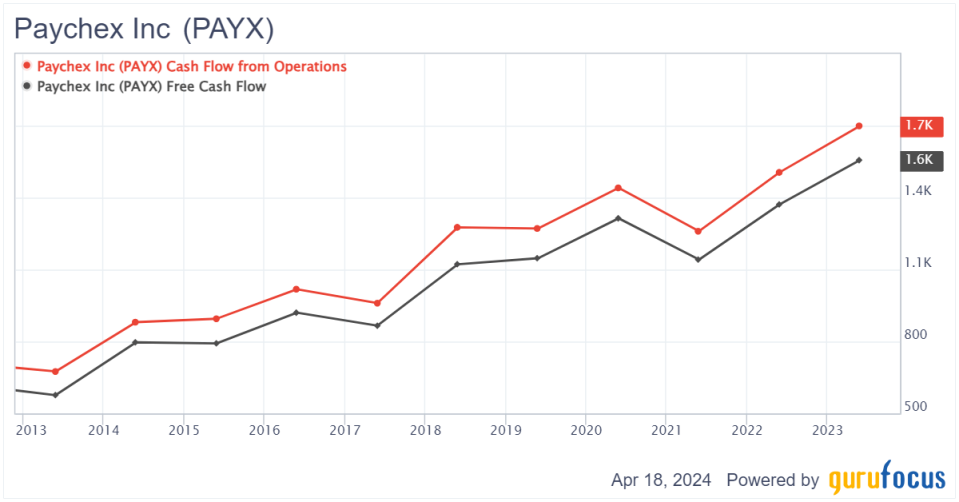

Paychex has very strong cash flow generation capabilities. Over the past 10 years, the company's operating cash flow has increased from $675.3 million to $1.7 billion. At the same time, free cash flow jumped from $576.6 million in 2013 to his $1.56 billion in 2023. Free cash flow margins have remained very healthy over time, staying between 24.79% and 32.52%.

Consistently high levels of cash flow generation and sustainable free cash flow margins allow Paychex to deploy significant cash, which is available to pay down debt, invest in growth, and return cash to shareholders through dividend payments and share buybacks. demonstrates the effectiveness of the business model.

PAYX Data by GuruFocus

High net cash level and low leverage ratio

Paychex has a robust balance sheet with a conservative capital structure. Through February, shareholders' equity was $3.75 billion, and cash and cash equivalents totaled nearly $1.7 billion. Interest-bearing debt balances amounted to just $818 million, giving Paychex a net cash position of $882 million. The company's debt-to-equity ratio remained very low at 0.22.

Investors may note that the largest asset item on Paychex's balance sheet is funds reserved for customers, which is approximately $6.08 billion. These “customer-held funds” refer to funds collected from customers but not yet disbursed for payroll taxes or employee wages. Given the purpose specified in the particular customer obligation, this fund is considered “restricted” and is prohibited from being used by Paychex for internal expenditures or investments. This should be maintained separately and used only for intended client-related functions.

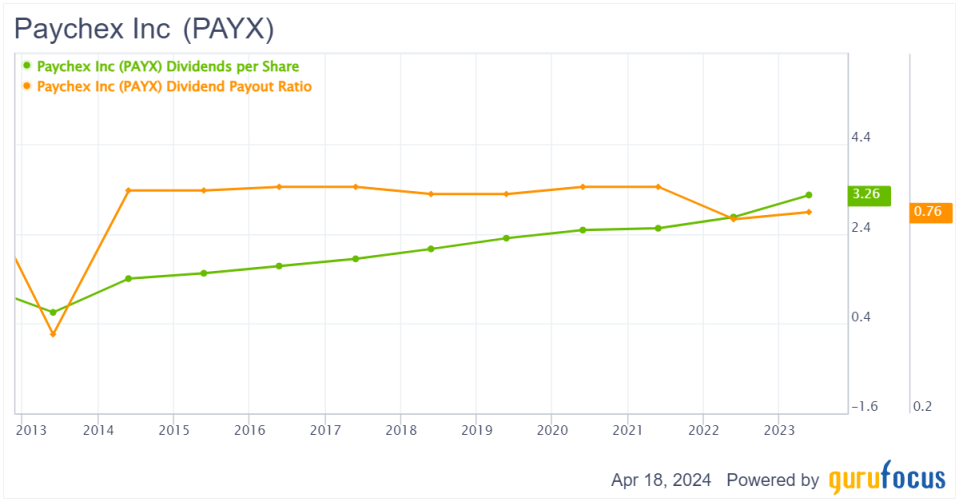

Stable dividend payments

Paychex has been very consistent in paying dividends to its shareholders. Since 2003, dividends per share have increased from 44 cents to $3.26 in 2023. Over the past 20 years, the dividend has only declined one year, from $1.27 in 2012 to 65 cents in 2013. Dividends have since risen again. At its current trading price, Paychex has a pretty good dividend yield of 2.70%, which is double the S&P 500's dividend yield of 1.37%.

To assess the sustainability of a company's dividend payments, investors should look at the payout ratio, which measures the percentage of a company's profits that are distributed to shareholders in the form of dividends. Over the past 20 years, Paychex's dividend payout ratio has hovered between his 0.42 and 0.95, demonstrating the company's strong commitment to paying dividends to its shareholders.

However, if the payout ratio reaches the high end of this range of 0.95x, it means that the company is paying out most of its profits during the year as dividends, leaving little for future growth. This may indicate alarm. The lower the ratio, the more sustainable the balance between shareholder returns and the long-term financial health of the company. In 2023, Paychex's payout ratio has settled to a more sustainable level of 0.76. With its growing business performance, stable cash flow generation, and reasonable payout ratio, we believe the chances of Paychex suspending its dividend payments are minimal.

PAYX Data by GuruFocus

is of considerable value

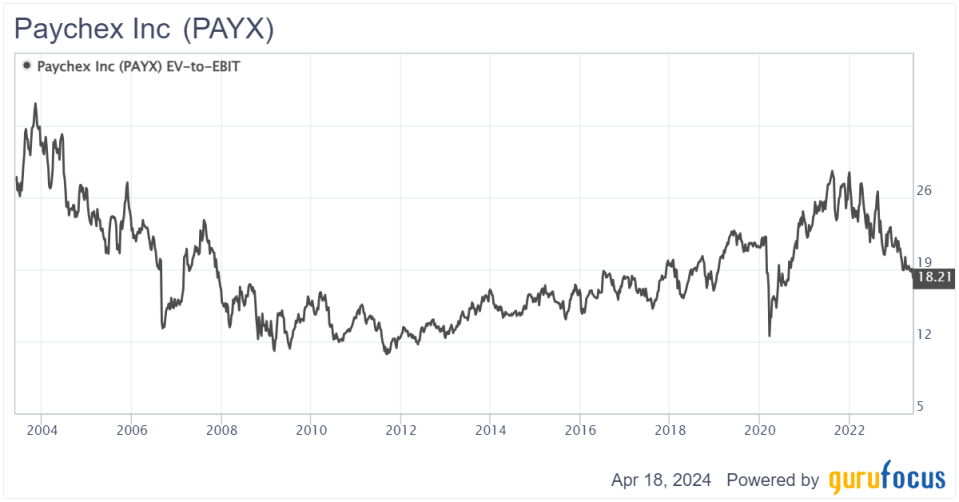

Since 2003, Paychex's Enterprise Value to Ebit ratio has fluctuated between 10.77 and 35.17. At the current trading price, the company is valued at a P/E ratio of 18.21x, slightly below the 20-year average multiple of 18.76x. Paychex therefore appears to be fairly valued when compared to its historical earnings valuation.

PAYX Data by GuruFocus

Paychex is expected to generate revenue of $5.55 billion in 2025. Assuming operating margins remain at 40%, operating income would be $2.22 billion. At an earnings multiple of 20x, the company's enterprise value would be $44.4 billion. Adjusted for its current net cash of $882 million, Paychex's stock value should be worth $45.3 billion. If there are 362 million shares outstanding, the intrinsic value per share is $125. Therefore, Paychex currently has a significant value in the market.

potential risks

Because Paychex's primary business is human resources services, its business is strongly tied to client growth, overall job creation, and economic growth. Therefore, if the Federal Reserve raises interest rates further, it will slow global economic activity, lead to job cuts, and harm the Federal Reserve's business.

Additionally, since Paychex's operating leverage advantage comes from its technology and Flex platform, the company should continue to reinvest in its business to innovate and enhance its technology. If a company is unable to adapt to a rapidly changing technology environment, customers may turn to a competitor's product. This is why Paychex requires the company to have a reasonable payout ratio of less than 0.70 in order to reinvest at least 30% of profits into future growth and keep the business sustainable.

conclusion

Over the past decade, Paychex has demonstrated commendable financial performance with strong operating results, including increased sales, operating income, and cash flow generation. The company maintains impressive operating margins that are significantly higher than its peers, indicating the company's efficient expense management and profitability. The company's balance sheet remains strong, with a strong net cash position and modest debt-to-equity ratio. Additionally, the company continues to return cash to shareholders through increased dividends. According to my analysis, Paychex has a good value in the current market. If the company can maintain a reasonable dividend payout ratio, it could be considered a decent investment opportunity for long-term income investors.

This article first appeared on GuruFocus.