")

eric vega

A few weeks ago, PENN Entertainment (NASDAQ:PEN) reported fourth-quarter results that disappointed investors. The games and entertainment company's stock price has fallen in response, hitting a 52-week low last week amid an intense sell-off. Based on the company's standards, Given recent financials and projections for the next two years, I think there is a good opportunity to enter a long position in Penn by selling the $15 put option.

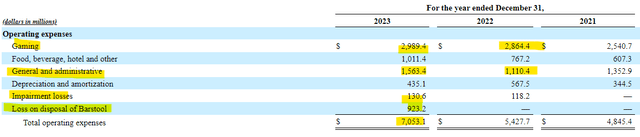

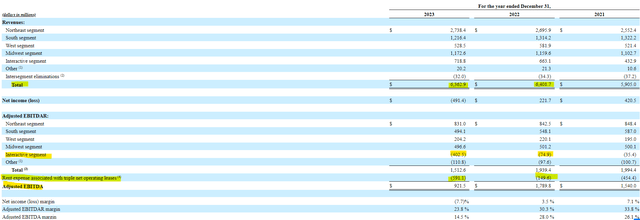

PENN Entertainment's full-year 2023 results were disappointing. The company saw a surge in food, beverage and hotel revenue to offset the decline in gaming revenue, but expenses rose significantly across all segments. Even without writing off Barstool, expenses still increased by $700 million. This resulted in adjusted EBITDA of $921 million, down from nearly $1.8 billion a year ago.

Section 10-K Section 10-K Section 10-K

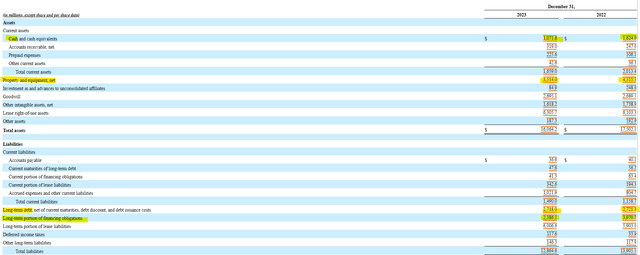

pen entertainment The balance sheet consists of $1 billion in cash and approximately $3.5 billion in hard real estate assets. The decrease in real estate assets is related to lease modifications entered into at the beginning of the year. The majority of assets are considered intangible, making shareholder equity tight enough to match market capitalization. During 2023, Penn expected long-term debt levels to remain stable at $2.7 billion, with financing obligations related to lease modifications reduced by more than $1.5 billion. The lease changes ultimately contributed positively to equity, but Barstool's amortization reduced equity to nearly $3.2 billion.

Section 10-K

The headwinds facing PENN Entertainment can best be seen by examining its cash flow statement. PENN Entertainment had operating cash flow of more than $800 million annually and free cash flow of more than $600 million for two consecutive years, but in 2023, operating cash flow decreased to $456 million and free cash flow It dropped to less than $100 million. Stock prices are under pressure due to declining cash flow.

Section 10-K

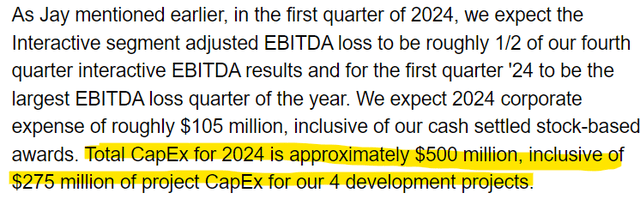

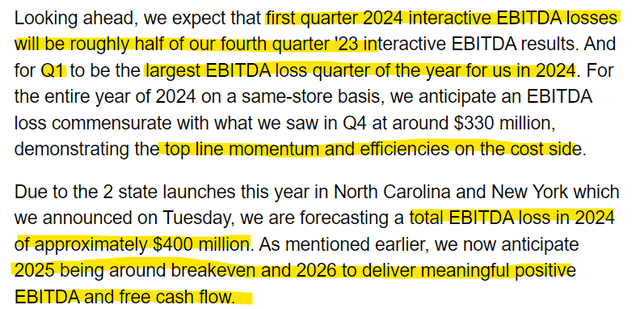

Looking ahead to 2024, PENN Entertainment's free cash flow could be around $0. This comes as he directed a $500 capital expenditure as he prepares to host the first March Madness on ESPN Bet and work on four of his other brick-and-mortar projects. Why should investors consider taking a position in the company's stock now, when the short-term outlook is so bleak?

earnings report

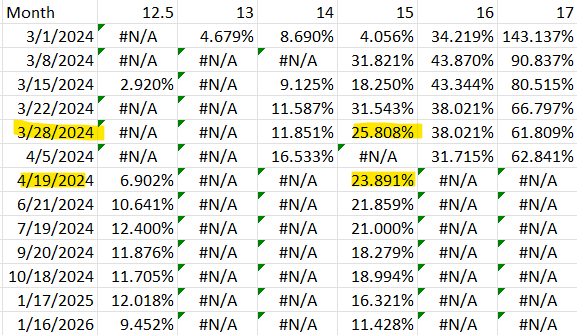

The current drop in stock prices has allowed option prices on discounted stocks to rise. For example, with a strike price of $15, a put investor who has secured cash could earn more than 20% annualized return without having to report any earnings between now and expiry. I prefer to get the March 28 expiration date, as March Madness data will likely not be available by then.

Yahoo Finance

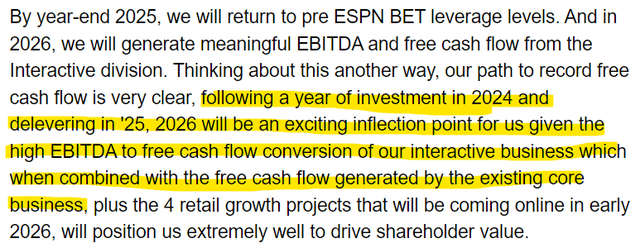

In addition to the options market, management is charting a path to strong earnings through the second half of 2025 and into the full year of 2026. Analysts are also expecting a strong recovery from next year. The stock currently trades at 13 times next year's P/E, but that multiple drops to closer to 11.5 times when the strike price of the option contract is taken into account. The timing would be perfect for the company to return to profitability and generate free cash flow in 2026, as the company has its next major debt maturing in the same year. If the company needs to burn cash in the future, it can use up his $1 billion in cash on hand.

earnings report Earn your transcript In search of alpha Section 10-K

PENN Entertainment's turnaround hinges on the execution of ESPN Bet and the timely (and on-budget) execution of its brick-and-mortar project. Despite the big hit to current earnings, the company's expansion prospects look bright. If I was given a $15 per share allocation, I believe that would be a great entry point for Penn stock. If not, selling put options can provide a good source of income.