's returns, and here's how they're trending")

If you're looking for a multibagger, there are a few things to keep in mind. One common approach is to look for companies that: Return value Capital employed increasing with growth (ROCE) amount of capital employed. Simply put, this type of business is a compound interest machine, meaning you are continually reinvesting your earnings at an ever-higher rate of return. Speaking of which, I noticed some big changes. Mr. Qualis (NASDAQ:QLYS)'s return on equity.

Return on Capital Employed (ROCE): What is it?

In case you aren't familiar, ROCE is a metric that measures how much pre-tax profit (as a percentage) a company earns on the capital invested in its business. The formula for this calculation in Qualys is:

Return on Capital Employed = Earnings before interest and tax (EBIT) ÷ (Total assets – Current liabilities)

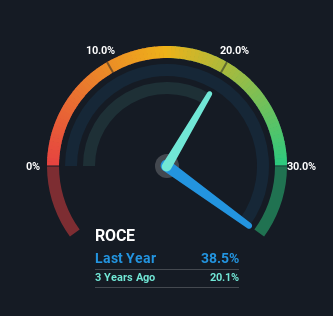

0.39 = USD 163 million ÷ (USD 813 million – USD 389 million) (Based on the previous 12 months to December 2023).

therefore, Qualys' ROCE is 39%. In absolute terms, this is a large gain, even better than the software industry average of 7.2%.

Check out our latest analysis for Qualys.

In the graph above, we measured Qualys' previous ROCE against its previous performance, but the future is probably more important. If you're interested, take a look at our analyst forecasts. free Qualys Analyst Report.

ROCE trends

Qualys' ROCE growth is quite impressive. More specifically, the company has kept its capital employed relatively flat over the past five years, while its ROCE has increased by 197% over the same period. Essentially, the business is generating higher profits from the same amount of capital, which is evidence that the company is becoming more efficient. However, this is worth considering more deeply. Because while it's great to see more efficiency in your business, it can also mean you lack areas to invest internally for organic growth going forward.

As a side note, the improvement in ROCE appears to be partially driven by an increase in current liabilities. Current liabilities have increased to his 48% of total assets, so he now has more funding from suppliers, short-term creditors, etc. And with current liabilities at this level, that's pretty high.

The conclusion is…

In summary, we are pleased to see that Qualys has been able to improve efficiency and earn higher returns on the same amount of capital. The impressive total return of 106% over the past five years shows that investors expect even better things to happen in the future. So, given that this stock has proven to have an encouraging trend, it's worth investigating the company further to see if that trend is likely to persist.

Qualys looks impressive, but no company is worth the infinite price tag. QLYS intrinsic value infographic helps visualize whether QLYS is currently trading at a fair price.

High returns are a key element of strong performance. free A list of stocks with solid balance sheets and high return on equity.

Have feedback on this article? Curious about its content? contact Please contact us directly. Alternatively, email our editorial team at Simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts using only unbiased methodologies, and the articles are not intended as financial advice. This is not a recommendation to buy or sell any stock, and does not take into account your objectives or financial situation. We aim to provide long-term, focused analysis based on fundamental data. Note that our analysis may not factor in the latest announcements or qualitative material from price-sensitive companies. Simply Wall St has no position in any stocks mentioned.