Embedded financing is a credit option so many Retailers and financial institutions deliver to customers to reduce friction and streamline purchases.

When a consumer checks out in-store or online they may be invited cover Purchase costs with a new credit card. Alternatively, you may be given the option to use Buy Now Pay Later (BNPL). Alternatively, your bank may extend the offer through its app.

Critically speaking, These options are embedded, So all this It can occur during checkout without directing the shopper to another site.

regardless of many ways Built-in financing options is presented For shoppers, PYMNTS Intelligence found that nearly half of consumers who purchased from a merchant or financial institution were very satisfied with the benefits.

That is one of the important discoveries contained in “.Built-in financing opportunitiesIt was produced at the request of “. visa and based on Based on a survey of more than 8,000 consumers in Australia, Germany, India, Japan, the UK and the US.

About half of consumers like the embedded offers they see. This is especially noteworthy. fact 43% of consumers said they would consider switching providers to take advantage of built-in financing options.

Another important discovery: Just under 23% of respondents said they would “never” use embedded lending, suggesting that more than three-quarters of consumers are at least considering using it.

Taken together, these insights mean half of consumers worldwide prefer embedded financing, 43% intend to switch merchants, and 75% are likely to accept embedded financing. embedded financing This represents a significant opportunity for merchants and financial institutions to expand their customer base.

If you need another reason, consider this exclusive data collected by PYMNTS Intelligence but not included in the final report.

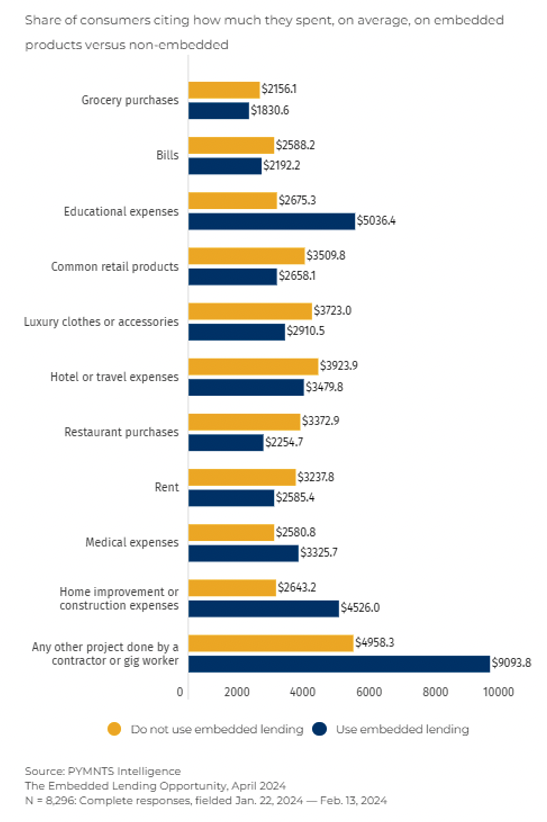

In some cases, consumers seem willing to spend more money when Take advantage of built-in financing.

for exampleWhen paying educational expensesconsumers who used traditional payment methods spent approximately $2,675, while those who chose built-in financing options spent more than $5,000. Similarly, consumers using embedded financing to pay for medical expenses spent $3,325, which was more than the $2,580 spent by traditional consumers. Those using built-in financing to invest in home improvement projects spent more than $4,500, while those using traditional payment methods only spent $2,643.probably the most important of all: Those who paid with loans built into contractors and gig workers spent nearly twice as much.

These findings suggest that some consumers are finding effective ways to offset short-term financial pressures associated with certain unplanned expenses, such as medical emergencies, home improvement projects, or unpredictable education costs. This suggests that they are considering embedded financing as a method.