Speaking of artificial intelligence (AI), we think of the “Magnificent Seven.” microsoft, apple, alphabet, Amazon, meta platform, teslaand Nvidia (NASDAQ:NVDA) — Gets the most attention from Wall Street.

Each of these companies is playing a key role in rapid changes across e-commerce, cloud computing, consumer electronics, robotics, advertising, and more. But of the Magnificent Seven, Nvidia may have the most important role. The company's graphics processing units (GPUs) power applications across the spectrum of generative AI, from machine learning and quantum computing to the data center.

At the 2024 Q4 earnings conference on February 21, NVIDIA CEO Jensen Huang declared that “accelerated computing and generative AI have reached a tipping point.'' With Nvidia stock up more than 230% in the last year, some investors may be wondering what Huang meant and whether it's too late to buy the stock. do not have.

Let's take a closer look at Nvidia's earnings report to assess the long-term trends driving demand for generative AI GPUs. Nvidia stock is certainly having fun right now, but investors may want to buy the stock now.

Nvidia's business is booming

When companies face unprecedented demand, revenues often skyrocket. That's all. In other words, companies may have to reinvest heavily in manufacturing to meet higher demand. This can put a strain on operating margins and margins, even during periods of accelerating sales growth.

But don't get me wrong, Nvidia is a rare breed.

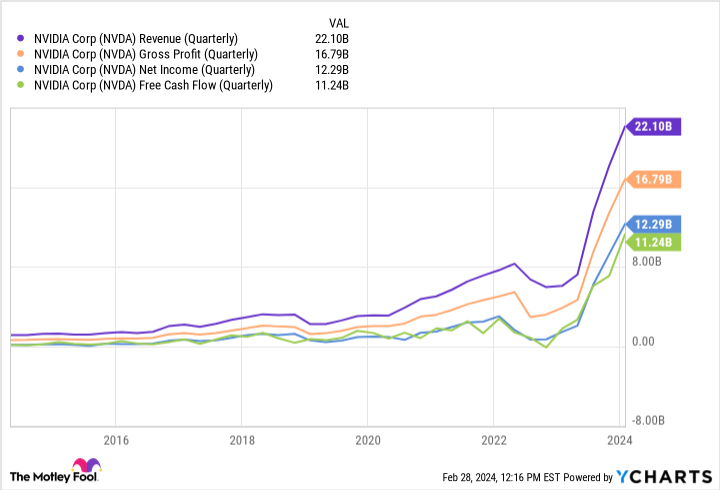

The chart above shows Nvidia's revenue, gross profit, net income, and free cash flow on a quarterly basis over the past 10 years. Look at how steep the slope of each line is. Not only is the company experiencing solid sales growth, but its profits and cash flow are also growing steadily.

Taking this a step further, Nvidia isn't resting on its laurels. Demand for his industry-leading A100 and H100 GPUs remains strong, but the company is relentlessly investing its profits in product innovation. The company plans to begin shipping next-generation chips, including the H200, in the second quarter. Additionally, reports say that Nvidia plans to release his B100, its most powerful chip to date, in the second half of 2024.

The above trends confirm the fact that Nvidia's chips are in high demand. And with a new and improved model set to be available to customers soon, Nvidia's efforts may just be getting started.

The AI revolution has just begun

As AI use cases continue to evolve, so too will estimates of the technology's total market size. A top manager at Nvidia recently predicted that the market for AI-powered chips and software will grow to a value of $600 billion. The jury is still out on whether that prediction proves accurate. But what analysts are looking for in terms of growth could reveal Nvidia's potential.

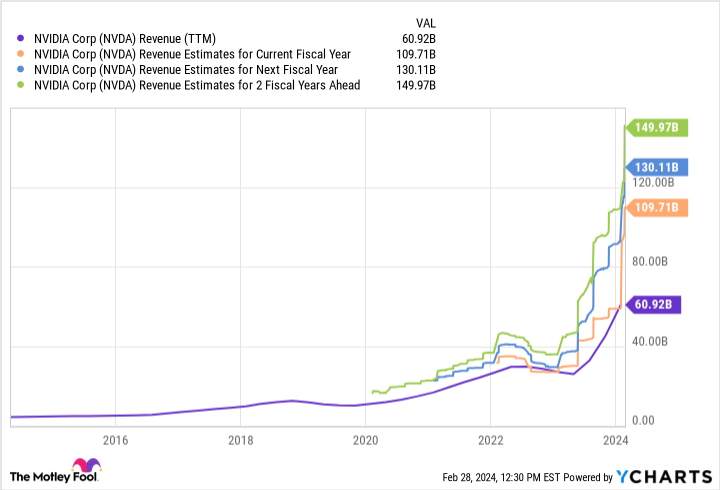

Nvidia's trailing 12-month revenue of $61 billion is impressive, but perhaps even more encouraging is the company's long-term growth prospects as estimated by Wall Street analysts. Considering his Nvidia's position as the market leader for AI GPUs, many clearly believe that current demand trends can be maintained for the next few years.

Is it too late to buy Nvidia stock?

To me, the biggest risk associated with Nvidia isn't its valuation. In fact, I think the competitive environment will become even more intense.His biggest rival at the moment is Nvidia. Advanced Micro Devices (AMD) However, Amazon and Microsoft are already developing their own inference and training chips for generative AI models. Nvidia may have a head start, but investors shouldn't turn their backs on the tech giant. I think it will take a few years for other chips to gain meaningful market share, but Nvidia investors should consider what growth drivers the company has other than his AI GPU. there is.

One area that investors may be overlooking right now is Nvidia's opportunity in software. Although the company is still primarily a hardware developer, Nvidia's software and services business reached a revenue run rate of $1 billion in the fourth quarter.

This is a big problem for several reasons. First, software tends to have high profit margins. If Nvidia eventually begins to lose share in the chip market, profit margins will likely take a hit. However, this could be more than offset if Nvidia continues to have success in the software space. Additionally, software services are typically more predictable in terms of demand, so I wouldn't be surprised to see investors place a further premium on Nvidia stock in the future.

With a price-to-sales ratio of 32, NVIDIA stock is trading well above historical levels. But the company's soaring sales and profits, combined with steady reinvestment in new products and an up-and-coming software business, could merit a premium. Given its differentiated business model, full-spectrum platform, and long-term tailwinds driving AI, I think now is as good a time as ever to pick up his Nvidia stock and hold it for the long term. Masu.

Should you invest $1,000 in Nvidia right now?

Before buying Nvidia stock, consider the following:

of Motley Fool Stock Advisor Our analyst team has identified what they believe Best 10 stocks What investors can buy right now…and Nvidia wasn't among them. These 10 stocks have the potential to generate impressive returns over the next few years.

stock advisor provides investors with an easy-to-understand blueprint for success, including guidance on portfolio construction, regular updates from analysts, and two new stocks each month.of stock advisor Since 2002, the service has more than tripled S&P 500 returns*.

See 10 stocks

*Stock Advisor will return as of February 26, 2024

John Mackey, former CEO of Amazon subsidiary Whole Foods Market, is a member of the Motley Fool's board of directors. Alphabet executive Suzanne Frye is a member of The Motley Fool's board of directors. Randi Zuckerberg is a former head of market development and spokesperson at Facebook, sister of Meta Platforms CEO Mark Zuckerberg, and a member of the Motley Fool's board of directors. Adam Spatacco has held positions at Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, and Tesla. The Motley Fool has positions in and recommends Advanced Micro Devices, Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, and Tesla. The Motley Fool recommends the following options: A long January 2026 $395 call on Microsoft and a short January 2026 $405 call on Microsoft. The Motley Fool has a disclosure policy.

Nvidia CEO says AI is at a 'tipping point'.Is the stock still a buy? Originally published by The Motley Fool