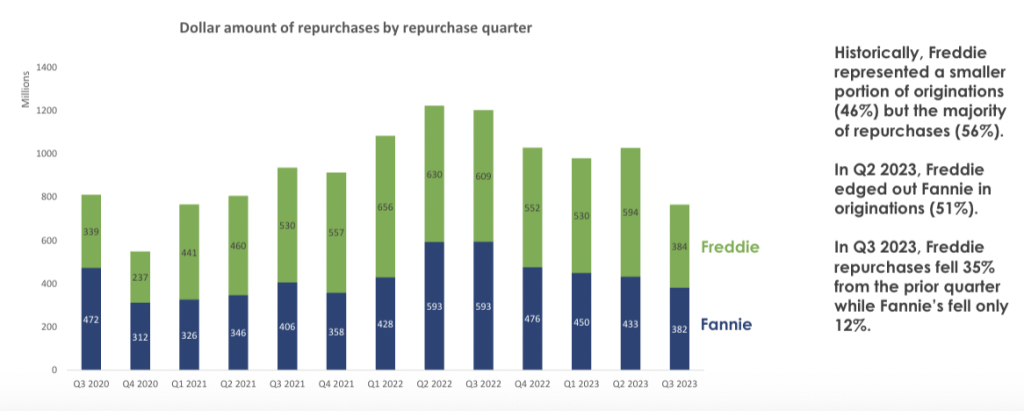

As of the third quarter of 2023, the most recent data available, Freddie Mac's repurchases were $384 million and Fannie Mae's repurchases were $382 million. However, the report notes that “Freddie's repurchases in the third quarter of 2023 were down 35% from the previous quarter, while Fannie's repurchases were only down 12%.”

Brett Ludden is a managing director and co-head of the financial services team at Sterling Point Advisors, an M&A advisory firm. He is also co-founder and managing partner of Augment Analytics.

“The overall trend is on the decline.” [loans] I bought it again [on a dollar basis]And that's true for both Fannie and Freddie,” Ludden said. “We expect both trends to continue.

“…but the data [for Q3 2023] shows that Freddy's repurchase rate is declining at a much faster pace [than Fannie’s]. …Once we get our fourth quarter results, we'll have more conclusive data at that point to see if the trend continues. ”

Report from urban research institute The study, which focused on repurchase rates on Fannie and Freddie loans, found that the GSEs in recent years have become “more aggressive, forced to repurchase more earlier in a loan's life than in previous vintages.” It is shown that there is a

According to an Urban Institute report released in November 2023, the average number of months from origination to repurchase from 2005 to 2008 (before and during the early stages of the global financial crisis) was 46 months for Freddie Mac and 46 months for Fannie. It was 52 months. May. However, from 2018 until the first quarter of 2023, the same numbers were 11 months for Freddie and 13 months for Fannie.

Crackdown on financing

Even though government agencies have become more aggressive in repurchasing loans over the past few years, especially in the wake of record loan volume growth in 2020 and 2021, the data shows that lenders also ensure quality control. This seems to indicate that they are becoming more vigilant about cracking down on loan origination (quality control).

ACES quality control, a fintech company that provides quality control software for the financial services industry, has published its Mortgage QC Industry Trends Report with data through Q3 2023. This report provides quarterly major defect rates for mortgage loans (primarily Fannie, Freddie, and Home Loans). federal housing administration loan) was analyzed via software.

According to the ACES report, the major defect rate decreased from 2.47% in Q3 2022 to 1.67% in Q3 2023. This is the latest data available. The report defines material deficiencies as deficiencies that “could render the loan uninsurable or unsellable.”

One of the ongoing QC efforts to stem loan repurchase demands by government agencies was launched by Fannie Mae in September of this year. The government requires companies that sell loans to the agency to complete a monthly pre-funding review for 10% of the previous month's loan origination amount or 750 loans, whichever is less.

Loan repurchase data from the GSEs is current through the third quarter of 2023, so it is still too early to determine whether Fannie Mae's program will have a material impact on repurchase demand.

“Stock buybacks are a hot topic for lenders, and these discussions have created a degree of bad publicity with agencies and investors,” said Nick Volpe., Executive Vice President of ACES Quality Control. “It's no surprise that investors want lenders to avoid as many problems as possible. [via QC efforts] before the loan is made.

“The most important goal of QC pre-funding is to avoid problems on closed loans before they occur. Problems are clearly bad loans that lead to repurchases or compensation.”

Non-QM alert

Pamela Hamrick, President In-center diligence solutionwhich provides due diligence screening and document management services to the mortgage industry, said pre-funding screening is also gaining attention in the non-qualified mortgage (non-QM) sector.

Non-QM loans are loans that cannot be purchased by GSEs. The pool of non-QM borrowers includes real estate investors, foreign nationals, business owners, gig workers, the self-employed, and a small group of homebuyers facing credit issues, such as past bankruptcies.

“We're seeing a lot more non-QM loans and DSCR (Debt Service Coverage Ratio) loans than we've seen in the past,” Hamrick said. “And these loans have historically been riskier than typical conventional loans.”

He added that an increasing proportion of non-QM lenders are “starting to accept more QC pre-funding qualifications as they have significant concerns about liquidity in the secondary market for non-QM and DSCR loans.” .

“If a lender closes a loan and an error is discovered, there is a good chance the loan will not be purchased,” Hamrick explained. “Therefore, screening your financing eligibility upfront will give you more certainty that your loan transaction will be successful.”

John Revonic is a senior partner at the law firm Garris Horn LLPserves the financial services sector, including mortgage companies, secondary market investors, quality control companies, and third-party review companies. He also previously served as CEO of Canopy, a third-party review company.

Mr. Revonic said that in today's market, the economics are shifting towards further incentivizing quality control review at the originator level.

“The assumption is that investors will price their loans better. [run through a quality control review] by the originator,” he added. “And when that happens, the investor buys the loan and also buys the right to due diligence through what is called a trust letter. This allows the investor to take the work done for the lender as if it were an investment. You can trust it as if it was done for your home.” [satisfying regulator and rating agency requirements].

“Therefore, lenders, regardless of size, are said to have to pay due diligence costs out of their own pocket, but then recover those costs through better execution.” [of the loan sale to the end investor]”

A&D Mortgage is an example of an originator that focuses on pre-funding quality control reviews. The company's head of capital markets, Alexander Saslov, said the originator performs pre-funding on 100% of A&D's entire loan production, including non-QM originations.

“We are 100% pre-funded, so we haven't had a very alarming number of loan repurchases,” Saslov said. “It was a small increase, but it was just a warning that we need to be more careful.” [in certain areas]”

future technology

Alan Qureshi, Managing Partner Blue Water Financial Technologies The technology solutions provider for the secondary mortgage market, which also provides risk management services, is excited about the future of tools such as artificial intelligence (AI) and digital quality control reviews that will help level the playing field in mortgage lending. He said he was holding her. It affects the market, including in terms of loan repurchases.

“Due to the nature of share buybacks and the non-standardization of loan disbursements, we have a fundamental problem with partner selection in a market where big companies get bigger and smaller companies get cut off, and that’s not good for companies.” ,” Qureshi said.

“The flip side is whether there are platforms that instead leverage technology (like AI and optical character recognition software (OCR)) to essentially level the playing field. It’s a good result and a solution.”

Vers Mortgage Capital We are an aggregator and affiliate of asset management and investment advisory companies. Invictus Capital Partners, sponsors non-governmental securitization platforms. Since its inception, Verus has acquired more than $30 billion in mortgage loans and completed 58 securitizations, according to the company. Dane SmithManaging Director and President of Vers.

“There are many stakeholders in the entire mortgage ecosystem, and due diligence is kind of a common thread, which allows… [loan] document [assembled in a PDF file] We need to turn it into a quality asset for institutional investors,” Smith said.

Smith also said that in an inherently high-volume, high-stakes business, advances in technology, including aspects of AI and OCR, can be expected to further improve the efficiency and accuracy of systems at all levels. But he emphasizes that the industry still has a long way to go to remove all human touch and judgment from the quality control process, which is essentially the bond of trust that binds the system together.

“We purchase loans from over 100 different mortgage banks every month,” Smith said. [generative AI] our system [non-QM] Guidelines. ”

He emphasized that AI systems are still under development and are not in common use at this time.

“We have trained users to ask questions and provide different guidelines in response,” Smith explained. “So we're closer together.” [to AI underwriting in the non-QM space]But I think there's still a long way to go before you can upload all your mortgage documents and understand the loan types, understand and accept the loan, and potentially run afoul of the guidelines. . .

“…There are many ways to use AI to improve productivity. Unfortunately, we are still far from decision-making, underwriting, and quality control.”