is in a strong position to grow its business")

It's easy to see why investors are attracted to unprofitable companies. For example, biotechnology companies and mining exploration companies often lose money for years before achieving success with a new treatment or mineral discovery. Nevertheless, only a fool would ignore the risk of a loss-making company running out of cash quickly.

Considering this risk, I decided to consider the following. Keypass Education International (ASX:KED) shareholders have cash burn to worry about. In this article, cash burn refers to the annual rate at which an unprofitable company spends cash to fund growth. Free cash flow is negative. Let's start by examining the company's cash compared to its cash burn.

Check out our latest analysis for Keypath Education International.

Does Keypath Education International have long fundraising power?

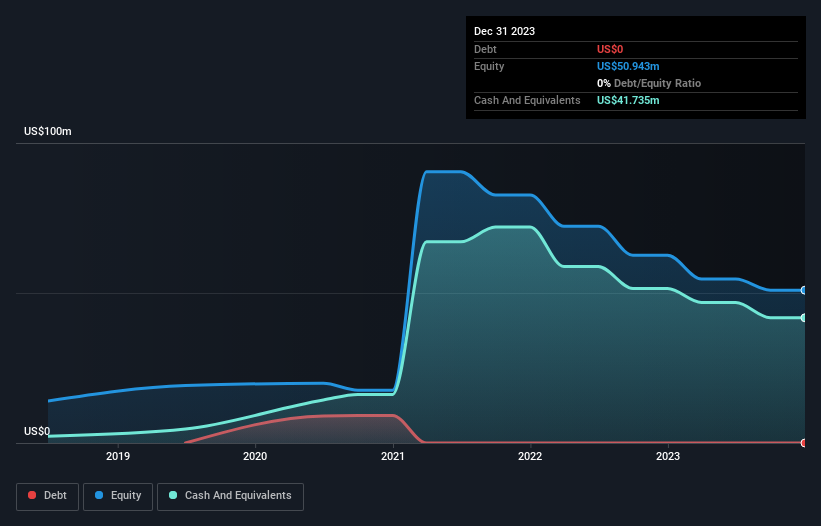

Cash runway is defined as the amount of time it will take for a company to run out of cash if it continues to spend at its current cash burn rate. As of December 2023, Keypath Education International had cash of his US$42m and no debt. Looking at last year, the company burned through US$9.5 million. Therefore, there was a funding period of approximately 4.4 years from December 2023. Notably, however, analysts think Keypath Education International will break even (on a free cash flow level) by then. If that were to happen, the length of that financial runway would be at issue today. You can see how its cash holdings have changed over time, as shown below.

How fast is Keypath Education International growing?

It's quite positive to see that Keypath Education International reduced its cash burn by 46% in the last year. Operating revenue also increased by 10%. Overall, I'd say the company is improving over time. However, it is clear that the key factor is whether the company will grow its business going forward. So it might be worth taking a peek at how much the company is expected to grow over the next few years.

How easily can Keypath Education International raise funds?

While we're certainly impressed with the progress Keypath Education International has made in the last year, we're also considering how much it would cost if we wanted to raise even more capital to fund more rapid growth. It's worth it. The most common ways for publicly traded companies to raise more money for their operations is by issuing new shares or taking on debt. Many companies end up issuing new shares to fund future growth. By comparing a company's annual cash burn to its total market capitalization, we can roughly estimate how many shares it would need to issue to run the company for another year (at the same burn rate).

Keypath Education International has a market capitalization of US$73m, so its cash burn of US$9.5m represents about 13% of its market value. As a result, we'd venture that the company could raise more cash for growth without too much trouble, even at the cost of some dilution.

So should we be worried about Keypath Education International's cash burn?

As you've probably noticed by now, we're relatively happy with how Keypath Education International is running out of money. In particular, we think the company's ability to raise funds stands out as evidence that it is spending well. Revenue growth is the company's weakest feature in this analysis, but that doesn't concern us. Shareholders will no doubt take great comfort in the fact that analysts expect the company to reach breakeven before long. After considering various factors in this article, we think the company is well-positioned to continue funding growth, so we're pretty relaxed about its cash burn. After a thorough risk review, we found the following: 1 warning sign for Keypath Education International What you need to know before investing.

If you want to check out another company with better fundamentals, don't miss this free A list of interesting companies with a high return on equity, low debt, or a list of growing stocks.

Have feedback on this article? Curious about its content? contact Please contact us directly. Alternatively, email our editorial team at Simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts using only unbiased methodologies, and articles are not intended to be financial advice. This is not a recommendation to buy or sell any stock, and does not take into account your objectives or financial situation. We aim to provide long-term, focused analysis based on fundamental data. Note that our analysis may not factor in the latest announcements or qualitative material from price-sensitive companies. Simply Wall St has no position in any stocks mentioned.