?")

It's hard to get excited about the recent performance of Data#3 (ASX:DTL), which has seen its share price drop 16% over the past three months. However, stock prices are usually driven by a company's financial health in the long run, and in this case it looks pretty respectable. In particular, I would like to pay attention to Data#3's ROE today.

Return on equity or ROE tests how effectively a company is growing its value and managing investors' money. More simply, it measures a company's profitability in relation to shareholder equity.

Check out our latest analysis for Data #3.

How do you calculate return on equity?

of ROE calculation formula teeth:

Return on equity = Net income (from continuing operations) ÷ Shareholders' equity

So, based on the above formula, the ROE for data #3 is:

58% = AU$41 million ÷ AU$72 million (based on the trailing twelve months to December 2023).

“Return” is the profit over the past 12 months. Another way to think of it is that for every A$1 worth of shares, the company was able to earn him A$0.58 in profit.

Why is ROE important for profit growth?

So far, we have learned that ROE measures how efficiently a company is generating its profits. Now we need to assess how much profit the company reinvests or “retains” for future growth, which gives us an idea about the company's growth potential. Assuming everything else remains constant, the higher the ROE and profit retention, the higher the company's growth rate compared to companies that don't necessarily have these characteristics.

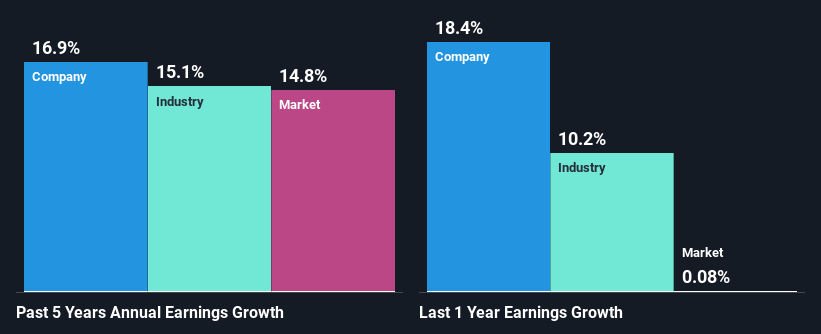

Data#3 revenue growth and ROE of 58%

First, we recognize that Data#3 has a very high ROE. Secondly, we can't ignore the comparison to the average ROE of 6.4% reported by the industry. This probably laid the foundation for Data#3's modest 17% net profit growth over the past five years.

As a next step, we compared Data#3's net income growth with the industry and found that the company has a similar growth rate when compared to the industry average growth rate of 15% over the same period.

The foundations that give a company value have a lot to do with its revenue growth. It's important for investors to know whether the market is pricing in a company's expected earnings growth (or decline). This can help you decide whether to position the stock for a bright or bleak future. If you're curious about Data#3's valuation, check out this gauge of its price-to-earnings ratio compared to its industry.

Is Data#3 making effective use of retained earnings?

Data #3's three-year median payout ratio is very high at 91%, which means that only 8.8% is left to reinvest in the business. This means that the company has been able to achieve decent profit growth even though it is returning most of its profits to shareholders.

Additionally, Data#3 has been paying dividends for at least 10 years. This means that the company is quite serious about sharing profits with shareholders. Based on our latest analyst data, the company's future payout ratio over the next three years is expected to be around 91%. Therefore, Data #3's future ROE is predicted to be 61%, which is also expected to be similar to his current ROE.

summary

Overall, we feel that Data #3 certainly has some positive elements to consider. In particular, the growth in earnings backed by excellent ROE is remarkable. Still, the high ROE could have been more beneficial to investors if the company had reinvested more of its profits. As highlighted earlier, the current reinvestment rate appears to be negligibly low. That said, the company's revenue growth is expected to slow, as predicted by current analyst forecasts. Learn more about the company's future revenue growth forecasts here. free Create a report on analyst forecasts to learn more about the company.

Have feedback on this article? Curious about its content? contact Please contact us directly. Alternatively, email our editorial team at Simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary using only unbiased methodologies, based on historical data and analyst forecasts, and articles are not intended to be financial advice. This is not a recommendation to buy or sell any stock, and does not take into account your objectives or financial situation. We aim to provide long-term, focused analysis based on fundamental data. Note that our analysis may not factor in the latest announcements or qualitative material from price-sensitive companies. Simply Wall St has no position in any stocks mentioned.