adam galt

Thursday's first-quarter GDP report delivered a one-two punch to markets: lower-than-expected growth and higher-than-expected inflation. As a result, stock prices fell and U.S. Treasury yields rose. At first glance, the risk-off response seems reasonable.However, a closer look at the GDP numbers shows that there is still room. for discussion.

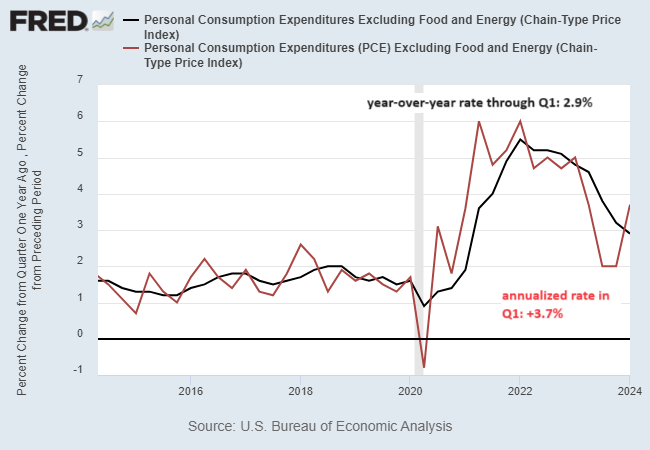

Let's start with the problematic data that has thrown the market into turmoil. That is the Personal Consumption Expenditure Price Index, also known as Core PCE, which excludes volatile food and energy prices, which is said to be the Fed's preferred inflation measure. On an annualized basis in the first quarter, the metric rose sharply by 3.7%, higher than expected. This is the news that sent the market into turmoil (red line in the graph below).

But when you look at the same data year-over-year, it looks even cooler. Notably, core PCE through the first quarter declined to 2.9% from 3.2% in the fourth quarter.1st quarter printing marks slowest pace Inflation will occur within 3 years.

More importantly, year-on-year indicators suggest that disinflation is still underway. Of course, the driver of the pullback is that the annualized value of core PCE is showing a sharp reflation phenomenon, which could indicate that price pressures are likely to intensify in the coming months .

An important question remains here. Which core PCE inflation is a more accurate indication of what is going on? The answer, of course, is that no one really knows, because the future is still unknown. That being said, I tend to prefer year-over-year trends when it comes to core PCE and other economic time series. why? It removes some, perhaps a significant amount, of the noise.

Of course, this time may be different, but history suggests that annualized measures of core PCE have a tendency to jump over one-year trends. Therefore, it is tempting to consider one-year trends as signals and quarterly annual measurements as noise. There are caveats to this view, but most of the time it tends to be true.

So if the one-year trend stops going down, or worse, starts going up, I'll change my view. At this point, neither situation seems likely, but I'm keeping a close eye on the numbers coming from different datasets for early warning that my assumptions are wrong.

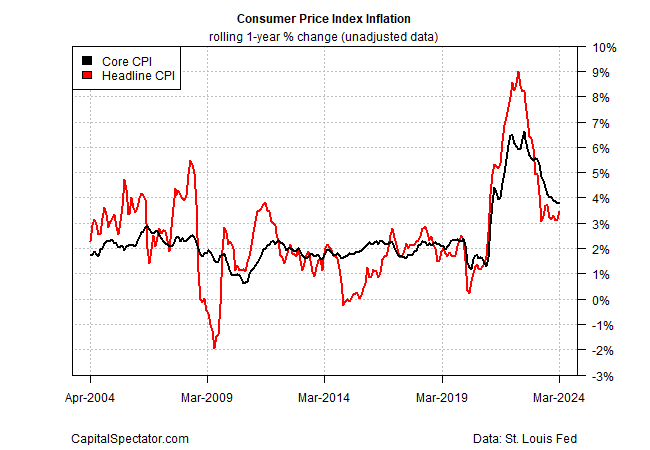

Also keep in mind that the hot core PCE data for Thursday's first quarter annualized data is old news. Recall that earlier this month we found that consumer price inflation rose at the headline level in March. However, year-on-year core CPI is still easing, albeit at a slower pace recently.

In conclusion, I still expect disinflation to continue until year-on-year changes in core PCE and core CPI level off or start to rise. There is room for debate about how and at what pace this will happen, but in the binary framework of “Is disinflation continuing?'' I'm still in the “yes'' camp.

original post

Editor's note: The summary bullet points in this article were selected by Seeking Alpha editors.