What GAO found

GAO estimated total annual direct economic losses to governments from fraud at $233 billion to $521 billion, based on data from fiscal years 2018 to 2022. This range reflects the varying risk environment during this period. 90% of estimated fraud losses fell within this range.

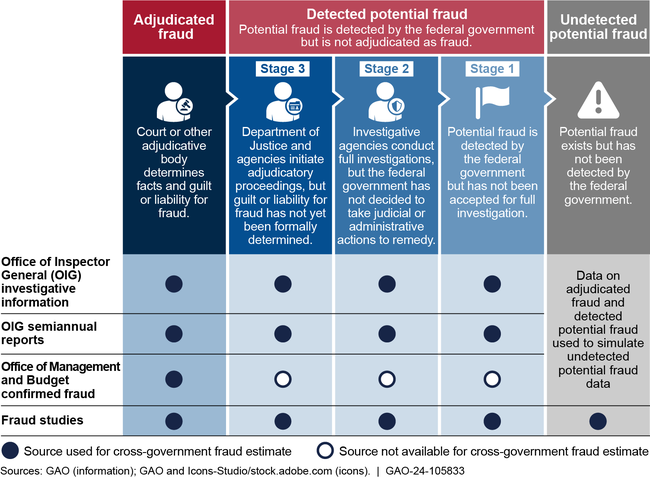

GAO collected data from three major sources to develop its estimates. One is investigative data, such as the number of cases sent for prosecution and the amount of money in closed cases. Office of Inspector General (OIG) Semi-Annual Reporting Information. We have identified fraudulent data reported to the Office of Management and Budget (OMB). GAO organized these data based on what he called three fraud categories: adjudicated, potentially detected, and potentially undetected. Model design and validation was also informed by 46 fraud studies. The OIG and other knowledgeable parties have agreed to these categories and subcategories.

Categories of fraud-related data used in GAO estimates

GAO's approach is sensitive to assumptions about fraud and takes into account data uncertainties and limitations. GAO used established probabilistic methods to estimate different outcomes under different assumptions and scenarios with uncertainties. This estimate does not include losses due to fraud related to federal revenue or fraud against federal programs that occur at the state, local, or tribal level unless investigated and reported by federal authorities. GAO's estimates are consistent with other fraud estimates by the United Kingdom and the Association of Certified Fraud Examiners, among others.

Although this is the first government-wide estimate of federal dollars lost to fraud, there are known uncertainties associated with the model and the underlying data that are important in interpreting the results. These include notes related to:

- Apply estimates to agencies and programs. GAO's model was developed to estimate federal fraud across the government. The estimated range of fraud is 3% to 7% of the average federal obligation. These percentages should not be applied at the agency or program level. All federal programs and operations are at risk of fraud, but the level of risk can vary widely. Reasons for changes in risk levels include budget management, expansion or contraction, and the emergence of new fraud schemes.

- Draw conclusions about pandemic fraud. GAO's estimates are based on data from fiscal years 2018 to 2022. Data includes time periods and programs with and without pandemic-related spending. Therefore, this estimate includes, but is not limited to, pandemic-related spending fraud. Although the upper bound of the estimate is associated with a high-risk environment, it is not possible to slice away a portion of the government-wide estimate to account for fraud in pandemic programs.

- Comparison with incorrect payment estimates. GAO's estimates are no match for inadequate payment estimates. Inadequate payment estimates are based on portions of federal programs that use methodologies not designed to identify fraud. GAO has also consistently reported that the federal government does not know the full extent of improper payments and has long recommended that agencies improve their reporting of improper payments. In contrast, GAO's fraud estimates include all federal programs and operations and are based on fraud-related data. Because of these differences in scope and data, the upper bound of GAO's estimated fraud range exceeds the estimated annual wrongful payments.and

- Assume that the estimates are predictive. GAO's estimates are not based on predictive models. Factors such as the amount of emergency spending, the effectiveness of federal fraud risk controls, and the nature of emerging fraud threats may have a significant impact on the magnitude of future fraud..

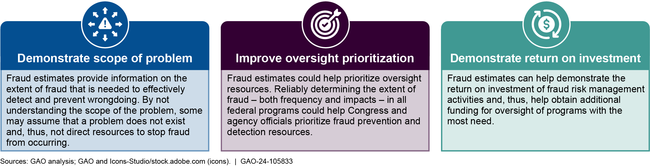

GAO has previously published recommendations for Congressional consideration and to improve the integrity of agency programs, including fraud risk management. According to OIG and agency officials, the presumption of fraud provides an opportunity to improve fraud risk management. For example, estimates can help indicate problem scope, improve monitoring prioritization, and determine return on investment from fraud risk management activities. While it is impossible to eliminate fraud, a better understanding of costs can help agencies better manage risk.

How fraud estimation can improve fraud risk management

OIG and agency officials noted challenges in developing fraud estimates, including the limited availability of fraud-related data and the use of different terms and definitions of fraud in recording the data. These data gaps and disparities make it impossible to easily compare or synthesize information to determine the extent of fraud across the federal government. Guidance regarding the collection and reporting of fraud-related data is currently limited to OIG semiannual reports and confirmed fraud reported by agencies to OMB, which are designed to support a presumption of fraud. Not designed. Guidance targeted to the purpose of presumption of fraud allows agencies and OIG to collect and report data on potential and adjudicated wrongdoing to support presumption efforts. You will be able to do it.

OIG and agency officials also noted the utility of agency- or program-level estimates compared to government-wide estimates. They further pointed out the need for specialized knowledge and data analysis ability to develop estimates. GAO previously reported that government agencies recognized limitations in expertise, data, and tools as significant challenges in fraud risk management efforts. These challenges can also impact an agency's ability to produce effective fraud estimates at the program or agency level. The Department of the Treasury's Office of Payment Integrity (OPI) supports agencies facing these challenges. OPI's resources are dedicated to preventing and detecting improper payments through a variety of data matching and data analysis services. Therefore, OPI has the expertise, data, and analytical tools to be well-positioned to assess and advance how the federal government can help manage fraud risk and estimate fraud.

Why GAO conducted this study

All federal programs and operations are at risk of fraud. Therefore, government agencies must have robust processes in place to prevent, detect, and respond to fraud. The government has mandated spending of approximately $40 trillion from fiscal years 2018 to 2022, but until now there have been no reliable estimates of fraud losses affecting the federal government.

As part of GAO's work on fraud risk management, this report (1) estimates the extent of annual direct economic losses from fraud, based on data from 2018 to 2022, and (2) Identify opportunities and challenges in fraud estimation to support risk management.

GAO used a Monte Carlo simulation model to estimate the range of annual direct economic losses from fraud based on data from 2018 to 2022. GAO identified opportunities and challenges through interviews and data collection focused on 12 agencies representing approximately 90% of the federal government's mandates.