Since Dell Technologies Inc.'s (NYSE:DELL) initial public offering in 2018, the stock price has increased approximately 530%. However, based on my operational analysis and detailed examination of its valuation and future growth projections, as well as thorough competitive comparisons, I believe this stock is not the wisest investment at this time. Based on the high momentum surrounding the artificial intelligence craze, I believe it could do incredibly well in the short term, but in the long term the market will correctly reassess its prospects and I believe the long-term price returns are not exceptional.

Dell’s AI journey

Dell's AI efforts generally focus on generative AI, AI-powered PCs, professional services, and collaborations with leaders in the space. Specifically, we introduced Dell Validated Design for Generative AI with Nvidia (NASDAQ:NVDA). It provides pre-trained models for data extraction without the need for organizations to develop their own, and Latitude series PCs integrate AI to improve productivity. , Collaboration, User Experience. Its wide range of AI products and services can be categorized as follows:

|

AI infrastructure |

Dell continues to develop infrastructure solutions for managing AI workloads. For example, we are evolving computing power, storage, and networking to support AI and machine learning. |

|

AI software and platforms |

Dell offers software solutions such as Dell EMC Ready Solutions for AI that simplify AI deployment through integration with hardware. |

|

AI collaboration |

Dell is working with major AI players such as Nvidia, VMware (VMW), and Pivotal (PVTL) to leverage advanced GPUs and integrate with leading software. |

|

AI research and development |

We are advancing AI capabilities in predictive analytics, machine learning for cybersecurity processes, and AI tools for data analysis and management. |

|

AI society/environment project |

Dell is committed to leveraging AI for social, environmental, medical, and educational purposes. For example, the company's AI tools are used to analyze data for climate change research. |

|

Training of AI human resources |

Importantly, Dell recognizes the importance of developing a workforce trained in AI tools and future demands. This includes working with top universities to offer courses in AI and machine learning. |

My view on Dell's AI business is that Dell offers a wide range of products and services and will undoubtedly be one of the key players in the advancement of AI across many industries in the coming years. That's what it means. I believe that preparedness in this region is not only wise, but vitally important. Furthermore, even if the initial costs are high, the large investment should benefit shareholders in the long term.

competition

Dell currently faces threats from nearly every major hardware provider. However, the scale of competition between companies varies, and after analyzing the competition, I believe that Dell offers a very promising strategy.

|

Hewlett-Packard (NYSE:HPQ) |

Use AI to improve security, performance, and user experience. The company has a division called HP Labs, which is a pioneer in AI research and development. |

|

Lenovo (LNVGY) |

Leverage AI across a variety of use cases, including smart devices, data centers, and customized business products. The company also incorporated AI into its manufacturing process to improve efficiency and reduce costs. |

|

IBM (NYSE:IBM) |

The company is deeply involved in AI, particularly through its Watson platform. It has been deployed in medical diagnostics, financial analysis, weather forecasting, etc. This software presents a challenge for Dell, especially in AI analytics and enterprise solutions. |

|

Acer (ACEYY) |

Acer isn't as involved, but it's incorporating AI to improve battery life and device performance. The company's threat to Dell is primarily in the consumer electronics market. |

|

Samsung (SSNLF) |

It has a comprehensive AI strategy that includes consumer electronics, Internet of Things, virtual assistants, and chip development. This is probably one of the major threats to Dell. |

When investing in companies related to AI, you need to remember that some companies have much higher returns than others. This is often because some companies are already large. For example, Salesforce (NYSE:CRM) and ServiceNow (NYSE:NOW) offer much higher potential rewards than Dell, albeit with higher risks as of this writing. What is most interesting about this new evolution in technology is that it is not only forcing historically dominant providers to adapt, but also bringing many new players on board.

Economic impact of AI

In my continued research into the AI market and technology developments, I find that the most dramatic change for technology companies and most industries is labor demand. It is reasonable to think that the increased use of AI and automation within companies will lead to fewer employees and leaner organizational structures. However, this may not be the case for leading models and will actually be a slow-growing endeavor.

Rather, what is most likely to occur is a restructuring of the job market. For example, Dell may have had many people working in manufacturing, but in the future much of that will be automated, reducing production costs through faster and more efficient processes and lowering consumer product prices. may be lowered. However, while human labor jobs in manufacturing may be eliminated, new roles should emerge in areas such as AI development, AI systems management, and creative thinking and design oversight, to name a few.

What I believe will happen in the future is not that the human job market will be phased out, but rather that the amount of work for the masses will increase from manual labor to knowledge work as the common form of human labor. That's true. This should increase profit margins primarily due to lower manufacturing costs, but not as dramatically as payroll expenses are phased out.

value analysis

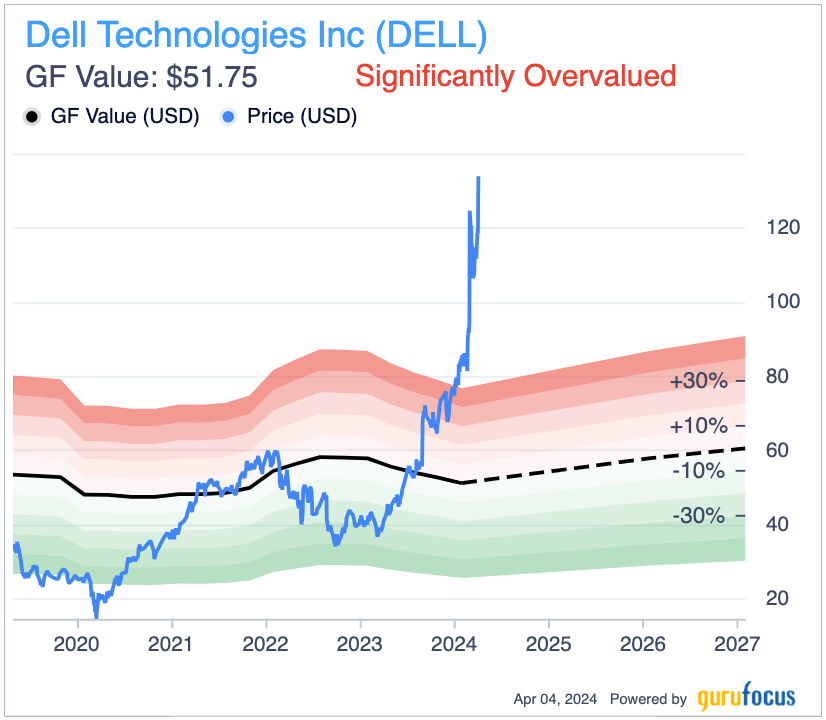

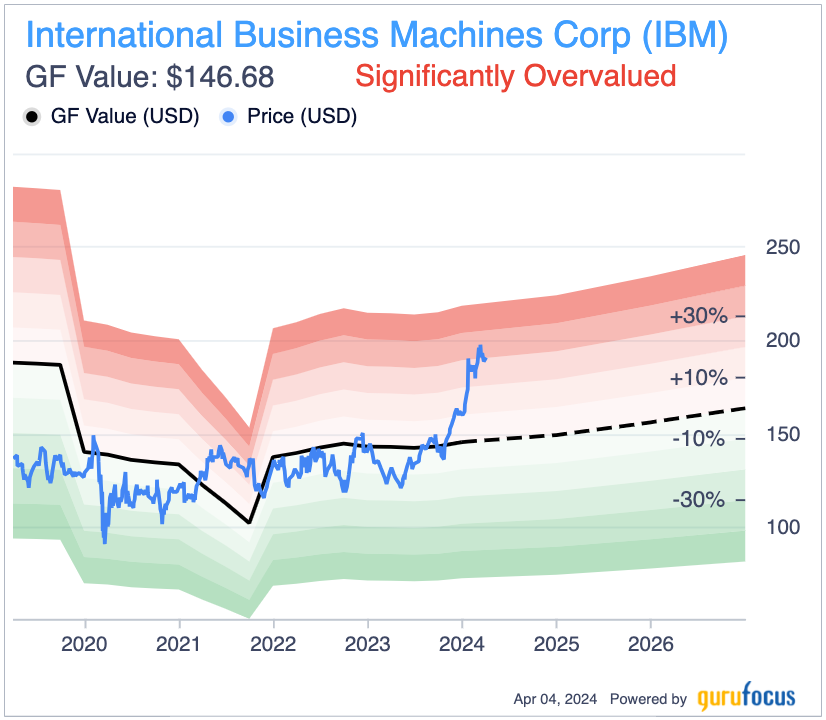

Overall, I think Dell has a similar investment case to IBM (NYSE:IBM). For example, based on the GF Value chart, Dell is considered significantly overvalued, while IBM is moderately overvalued.

Over the next three years, Dell expects its earnings per share, excluding non-recurring items, to grow at a compound annual rate of 6.53%, while IBM expects it to grow at a CAGR of 4.66% over the same period. What's clear here is that not only are investors getting a relatively low growth rate based on consensus estimates, they're probably not getting good value either. This shows that artificial intelligence is not a panacea. Just because a company uses it a lot doesn't mean it will drive rapid growth. In my opinion, it is far more prudent to look at AI as an optimizer of growth rather than as a source of growth itself. Therefore, companies that are already experiencing high growth will benefit the most.

I categorized six peer companies in a table and compared their earnings consensus estimates and price-to-earnings ratios at the time of writing.

|

Dell |

HP |

lenovo |

IBM |

acer |

samsung |

|

|

3-year EPS CAGR consensus |

6.53% |

0.81% |

5.84% |

4.66% |

7.42% (2 years') |

45.68% |

|

PER |

July 20th |

8.07 |

April 16th |

19.86 |

28.45 |

39.35 |

Revenues do not include non-recurring items

Median PE of hardware industry excluding NRI ratio = 22.84

From this table, it is clear that Samsung has a very high short-term future growth rate, but I am skeptical about how likely it is that it will be able to maintain this growth rate over the next 10 years. Although Dell's price-to-earnings ratio is high, consider that the company's valuation multiple is lower than his IBM, and the consensus on earnings forecasts for the next three years is stronger. In my opinion, Acer is definitely the weakest among its peers from a profitability-based value and growth perspective.

balance sheet risk

Investors who are familiar with Dell will know that my biggest concern about the company at this point is its negative balance sheet with an equity ratio of -0.03. The median value over the past 10 years is -0.01, and the maximum value is only 0.11. To me, this is very worrying especially for his company founded in 1984.

This company may be good operationally, but I think there is some work to be done in terms of financial management. With such a weak balance sheet, I think it's extremely unwise for management to buy back so many shares every year since 2017. As such, I think management should seriously consider reducing its share repurchase program in order to refocus on strengthening its balance sheet and repaying its debt. Total debt stood at $25.99 billion as of the last report.

Further risks that may hinder progress

Given that Dell is likely overvalued at this point, it's also important for potential investors to understand the risks associated with Dell's involvement in AI at the time of this analysis. As Catherine Wood (Trade, Portfolio) of Ark Investment Management stated, I believe that great start-ups will emerge with significant levels of new innovation, effectively disrupting the established balance of power. We should keep this in mind. Dell will likely face high-growth competition in the form of new hardware companies, some acquired by larger companies and others remaining independent. This is already evident in the enterprise products mentioned above, such as Salesforce and ServiceNow, but it is also evident in the range of cybersecurity companies that are making significant investments and integrations in AI, and are increasing Dell's approach to hardware and software security. may thwart in-house efforts.

It is worth remembering that the cybercrime market will evolve dramatically with new criminal capabilities from advanced technologies, such as the ability to crack codes and passwords with quantum computing. As a result, the cybersecurity sector is also leveraging quantum computing to establish robust security measures for organizations and their customers. I think it's inevitable that Dell will need to collaborate and outsource some of these advanced tasks, and I'm particularly active in doing so. I commend you for that. However, concerns remain about the growth prospects for certain sectors of AI-driven tools.

conclusion

In summary, Dell is currently very well positioned in the AI market and should benefit from the positive effects of consolidation, particularly in terms of business efficiency and long-term pricing.

However, I believe it is fair to consider the stock to be overvalued. As such, there are many competitors in this space in particular, some of which offer very attractive investment prospects with consensus high growth potential far exceeding what Dell is offering. Considering that there is, I would not invest. My rating on this stock is Hold as I believe it has the potential to perform broadly in line with the broader S&P 500 index over the next 10 years.

This article first appeared on GuruFocus.