stock, poised to rise 100%, but it's incredibly cheap right now")

Its important role is Nvidia (NASDAQ:NVDA) Thanks to the huge computing power of graphics processing units (GPUs), which are contributing to the proliferation of artificial intelligence (AI) technology, the company has witnessed a notable spike in sales and earnings in the last few quarters. It explains why.

Revenue for the recently ended fiscal year 2024 increased 126% to $60.9 billion. Analysts are predicting a strong 96% increase in revenue this fiscal year, to $110.6 billion. Meanwhile, analysts expect the company's revenue to double this year, but the company enjoys tremendous pricing power in the AI GPU market, so it could outperform on this front. There is.

All of this suggests that Nvidia should be able to justify its lofty valuation. The company has a price-to-earnings ratio of 75x, but looking at his 35x forward earnings shows how quickly earnings are expected to grow. Additionally, NVIDIA's price-to-earnings (PEG) ratio is just 0.13. A PEG ratio of less than 1 is considered to indicate that the stock is undervalued relative to its expected growth.

But cautious investors who have doubts about Nvidia's growth story may be wary of buying Nvidia at such a valuation after the stock has risen 225% over the past year. However, for investors who are currently looking to buy value plays in the AI field, Dell Technologies (NYSE:Dell) Looks like an ideal stock pick.

Dell Technologies has several AI-related solid catalysts

Dell's business consists of two segments. The first is Infrastructure Solutions, through which the company sells storage and server solutions along with networking products and services. The second segment is Client Solutions, which includes sales of workstations, personal computers (PCs), and other peripherals.

The good news for Dell investors is that both of these areas are on track to greatly benefit from increased adoption of AI.

The company's infrastructure business is growing significantly due to sales of AI servers used to install chips from companies such as Nvidia. In Dell's fiscal fourth quarter of 2024 (ending February 2nd), the Infrastructure Solutions segment's revenue was $9.3 billion. This was down 6% year-over-year, but up 6% quarter-over-quarter due to increased demand for AI-optimized servers.

Dell shipped $800 million worth of AI servers during the quarter. This metric is likely to rise further as AI server orders increased 40% from the previous quarter and Dell's AI server backlog reached his $2.9 billion. Its AI server-related order book is sure to continue to grow. According to Global Market Insights' forecasts, AI server market revenue will jump from $38 billion in 2023 to $177 billion in 2032.

The company is already seeing “strong order interest” for next-generation chips from Nvidia and NVIDIA. Advanced Micro DevicesThis indicates that orders for AI-specific servers are likely to increase further in the future.

Similarly, Dell expects the advent of AI to improve its client solutions business, which has been under stress due to declining PC sales. Client Solutions revenue was $11.7 billion in the fourth quarter, down 12% from the year-ago period. However, the subsequent decline was only 5%.

“PCs will become even more essential as most of our daily tasks using AI will be done on PCs,” Dell Chief Operating Officer Jeffrey W. Clark said in February. This was stated at the financial results conference on the 29th. To capitalize on this opportunity, the company has already announced a new line of commercial PCs with integrated AI capabilities. This is a smart move as he is expected to see more AI-powered PC shipments this year.

Market research firm Canalys predicts that AI-enabled PC shipments will reach 48 million units in 2024, 100 million units in 2025, and 205 million units in 2028. Canalys also notes that AI PCs will likely carry a 10% to 15% price premium. % compared to traditional PCs. Given that Dell is the third largest PC OEM and will control just over 15% of this market in 2023, it stands to benefit from this fast-growing niche market.

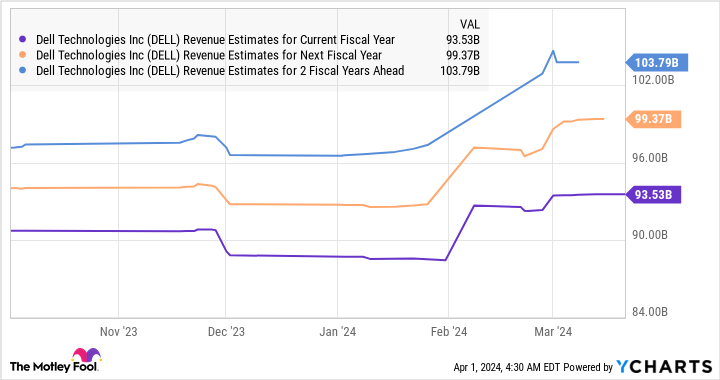

These AI-related catalysts explain why analysts have significantly increased Dell's revenue growth expectations recently.

Valuation and upside potential make this stock a good buy now

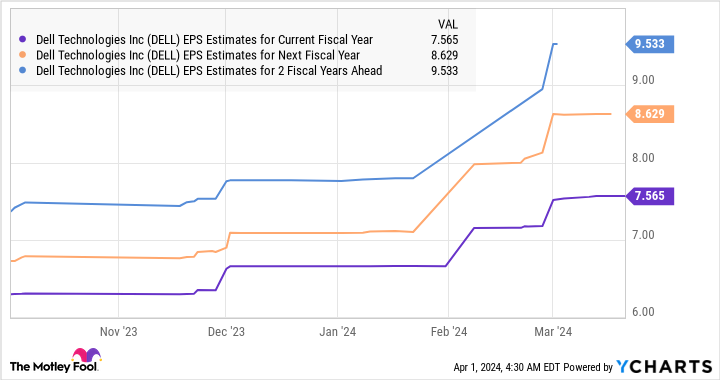

Dell's top-line performance is expected to improve over the next three fiscal years, and that revenue growth is expected to be reflected in its bottom line.

Dell currently trades at just under 25 times its price-to-earnings ratio. The expected earnings multiple is even lower at 15.7x.For comparison, we used a lot of technology. Nasdaq-100 The index has a year-end earnings multiple of 31x and a forward earnings multiple of 27x. Assume that the company delivers him $9.53 in earnings per share in his 2027 fiscal year, at which point he trades at 27 times earnings (using the Nasdaq 100's forward earnings multiple as a proxy). use). tech stock), whose stock price could soar to $257 within three years.

This would be a 100% increase from current levels. Dell is already up 210% over the past year, but don't be surprised if this tech stock continues to see impressive gains due to its improved AI track record. So investors looking to buy a growth stock that isn't ridiculously expensive should consider adding Dell Technologies to their portfolio before the stock price skyrockets.

Should you invest $1,000 in Dell Technologies right now?

Before buying Dell Technologies stock, consider the following:

of Motley Fool Stock Advisor Our analyst team has identified what they believe Best 10 stocks What investors can buy right now…and Dell Technologies wasn't among them. These 10 stocks have the potential to generate impressive returns over the next few years.

stock advisor provides investors with an easy-to-understand blueprint for success, including guidance on portfolio construction, regular updates from analysts, and two new stocks each month.of stock advisor Since 2002, the service has more than tripled S&P 500 returns*.

See 10 stocks

*Stock Advisor will return as of April 1, 2024

Harsh Chauhan has no position in any stocks mentioned. The Motley Fool has a position in and recommends Advanced Micro Devices and his Nvidia. The Motley Fool has a disclosure policy.

Did you miss Nvidia's incredible growth spurt? It could be the next big artificial intelligence (AI) stock, has a potential return of 100%, and is incredibly cheap right now