eren 11

There were early signs of tightening financial conditions in the market as higher interest rates and a stronger dollar pushed up inflation while stalling the disinflationary process.

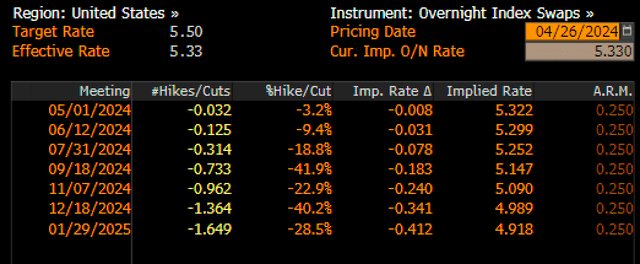

Jay Powell will likely repeat his previous message that inflation is certain to fall. process stopped At this week's FOMC meeting. The latest PCE report shows several signs of problems, including: PCE super core accelerates This is the fastest pace since January 2023.

This week is packed with employment data, with the first quarter employment cost index released on Tuesday and ending with the BLS employment status report on Friday. This week's data will tell us whether rising yields and a strong dollar are here to stay, or whether current trends have gone too far and need to be reversed.

Interest rate and dollar technicals both suggest that dollar levels remain much higher. It appears that the recent trend of tightening in financial conditions has only just begun. But of course, Wednesday's FOMC meeting will give the market the green light to proceed or pause, depending on the situation, and will give a signal for stocks to go up or down.

data dump

The employment cost index will be released on April 30 and is expected to rise at a seasonally adjusted annual rate of 1% sequentially in the first quarter, up from 0.9% in the fourth quarter. Then, on May 1, the ADP Employment Change Report was released, and the number of jobs created in April is expected to be 180,000, down from 184,000 in March. Meanwhile, the JOLTS report, also released on Wednesday, predicted that the number of job openings in March would decline to 8.68 million from 8.76 million in February. Also on Wednesday, the ISM manufacturing report is expected to show the sector continues to expand, but falls from 50.3 to 50.1. But more importantly, the ISM price paid index is expected to fall from 55.8 to 55.2.

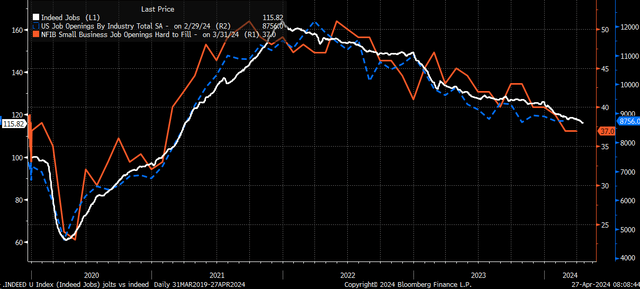

In fact, job data shows that the number of vacancies continued to decline from March to April, while NFIB vacancies remain at the bottom of the list as they are difficult to fill. This means that the decline in JOLTS is probably consistently decreasing, indicating that the labor market continues to ease.

bloomberg/certainly

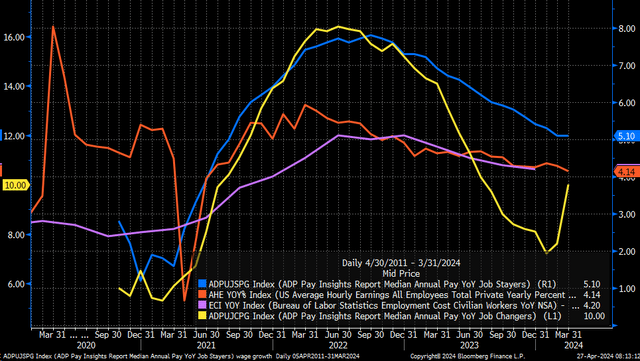

Meanwhile, both the ADP and BLS suggest that wage growth continued to slow in the first quarter, but at a much slower pace than in the previous quarter. Wage growth may even be slightly higher, as current analysts' estimates of his ECI suggest. What will be interesting to watch in this week's April ADP report is whether wages continue to rise for workers who find new jobs. The rate jumped from 7.6% in February to 10% in March.

bloomberg

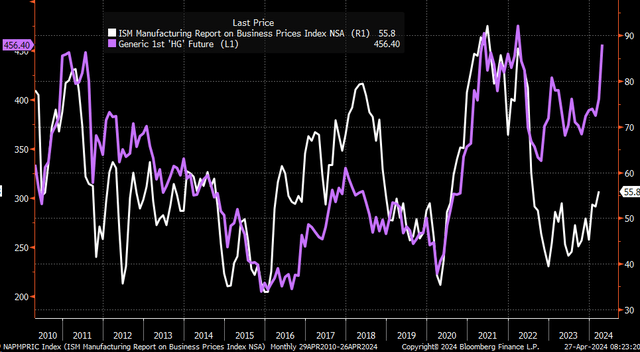

The price paid index for ISM manufacturing may be more important than whether the sector has expanded. The ISM Report's Price Paid Index is highly correlated with commodities such as copper, and copper prices rose dramatically in April, so a higher-than-expected number in the ISM Price Paid Index is not surprising.

bloomberg

Non-agricultural productivity is expected to slow on Thursday to 0.8% in the first quarter, down from 3.2% in the fourth quarter. Meanwhile, unit labor costs are expected to rise to 3.3% from 0.4% in the fourth quarter.

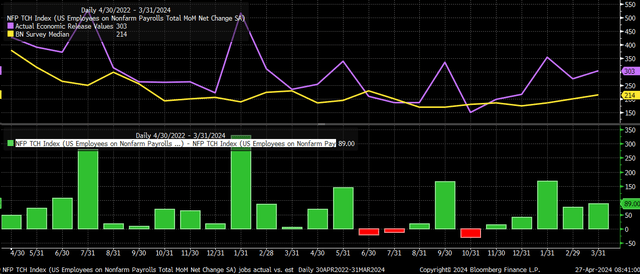

Employment data will be released on Friday and is expected to show non-farm payrolls increased by 250,000 in April from 303,000 in March, but the unemployment rate remained at 3.8%. There is. The average hourly wage is expected to remain unchanged at 0.3% from the previous month, while the year-on-year comparison is expected to decline from 4.1% in March to 4.0%.

Analysts have been under-predicting job creation in the past few months. Since April 2022, analysts have overestimated the number of jobs created in just three out of 24 reports.

bloomberg

PCE numbers were even higher last week, while GDP fell below Wall Street estimates and models from the Atlanta Fed and others. However, the PCE report surprise was enough to push 10-year rates up 4bps. By comparison, the two-year bond rose about 1 basis point. Furthermore, the market had priced in the expectation of a rate cut, and the first rate cut was not implemented until December.

bloomberg

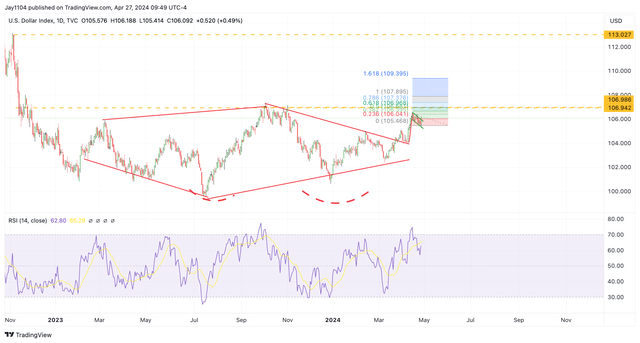

Higher interest rates, stronger dollar

Technical analysis still points to the 10-year Treasury rate rising above the resistance level of approximately 4.65% and not rising until the next significant resistance level is 5%. One significant risk is the Treasury's quarterly repayment announcement scheduled for May 1 at 8:30 a.m. However, the bid size is not expected to change and it is not expected to be as big an event as the past few quarters. .

TradingView

Meanwhile, the dollar index continues to show bullish trends and now appears to be coming out of a short-term bull market. This suggests that the dollar index will rise in the coming days to weeks, rising above the resistance near $107 to a high of $107.90. This would put the dollar on track to return to 113 on the index.

TradingView

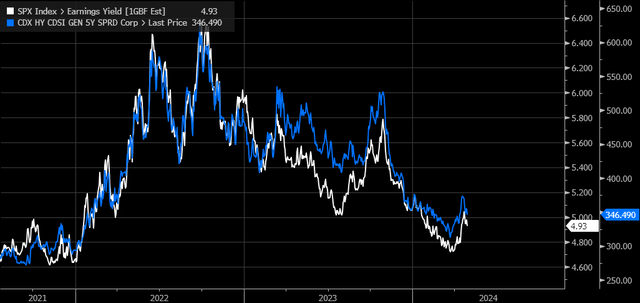

Higher interest rates and a stronger dollar will keep the CDX High Yield Spread Index higher, and the Fed's confirmation at Wednesday's FOMC meeting that a rate cut is unlikely and inflation is stagnant will push the spread further. It will expand.

bloomberg

The S&P 500 Index has long traded on credit spreads, so if interest rates rise, the dollar strengthens, and spreads rise, the S&P 500 Index's earnings yield should rise. This would suggest that financial conditions are tightening and that stock prices will continue the downward trend that began several weeks ago.

bloomberg

Of course, this all depends on the data, and if the data is weaker than expected, yields will fall, the dollar will fall, spreads will fall, and stock prices will rise. But at the moment, technical analysis suggests higher interest rates and a stronger dollar, which means wider spreads (widening) and lower stock prices because economic fundamentals are overheating, so will need to tighten monetary conditions to prevent inflation from spiraling out of control again.