Phong Lamai Photo/iStock, Getty Images

Remember when Marty's father was fired in 2015 in Back to the Future? It wasn't a text or an email. It was a fax! The film got a lot of things right, including the drones and video conferencing, but it missed his two most transformative developments. The next decade: Mobile phones and the Internet. The problem with many predictions about technology is that they are wildly off the mark.

Some historically bad calls

1943: The president of IBM (IBM) predicted worldwide demand. perhaps 5 computers.

1995: Newsweek publishes an op-ed by astronaut Clifford Stoll predicting that the Internet will never replace print newspapers and significantly downplays the potential of electronic commerce. Amazon (AMZN) reported $232 billion in revenue from online sales last year.

2007: Former Microsoft CEO Steve Ballmer predicted that there was “no chance that the iPhone would make any significant progress.” Market share” Apple (AAPL) has approximately 1.5 billion users and $386 billion in 12-month (TTM) revenue.

2008: Oracle (ORCL) CTO calls cloud “complete nonsense.” Amazon and Microsoft (MSFT) reported that Amazon Web Services (AWS) and Microsoft Intelligent Cloud revenue in the previous year was $91 billion, $88 billion. Oh, and Nvidia (NVDA) is worth more than $2 trillion thanks to surging data center sales.

What's the point?

Everyone talks bad about the future, including experts. It's hard to predict where technology will go, and many of us (including myself!) resist the hype of new things.

Importantly, we tend to underestimate how much new technology will impact our daily lives. I remember when the internet came out. Although it was pretty, it had little practical use. Dial-up was incredibly slow and unreliable, and once connected there was nothing to do.

But technology is always moving towards something more convenient and efficient, like e-commerce. It took a while, but in hindsight it's obvious.

This is what I think when people discount the potential of artificial intelligence (AI) in the business world and in our favorite stocks. There will be many failures and false starts along the way., but technology is coming. The IMF predicts that 40% of global employment will change. Perhaps in time there will be more.

Some stocks fall into bubble territory and fail miserably in the long run, while others are hugely successful. He doesn't put all his eggs in one basket, and he doesn't put them all in all baskets. However, here are some things to consider and why.

arm holdings

Arm (ARM) Holdings is a chip company that doesn't make chips. The company designs what it calls the CPU and GPU “architectures” that power smartphones, data centers, advanced driver-assistance technologies, and more. The company claims that it has shipped a total of 280 billion units and that 99% of the world's smartphones use its CPUs.

There are several reasons why I like this company.

- Because the company is not a manufacturer, its gross profit margin is over 95% and its free cash flow margin is close to 30%.

- It has a strong balance sheet with current assets of $3.6 billion and current liabilities of $866 million.

- Its market share is increasing in many industries.

- Remaining performance obligations (RPO) increased 38% sequentially to $2.4 billion.

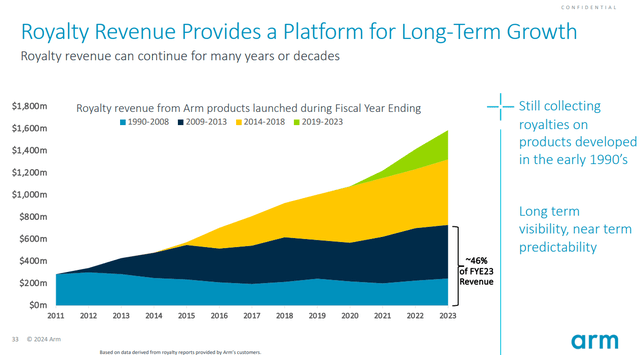

The best part about this business model is that royalty income accumulates as new products are introduced while legacy products continue to be used, as shown below.

arm holdings

Legacy income is great. Research and development costs are paid years in advance, so they are very profitable.

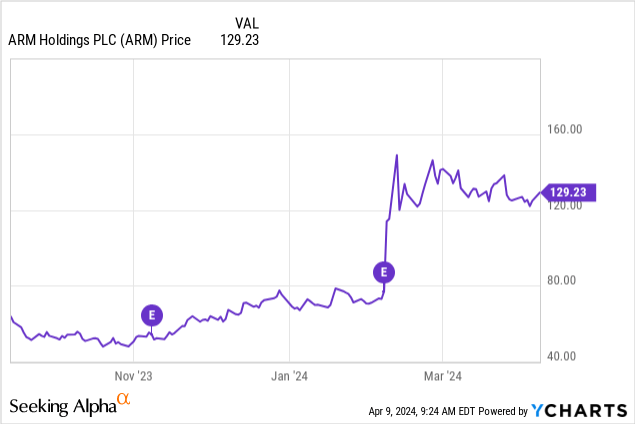

As you can see below, Arm stock soared after last quarter's earnings release, so there could be a short-term correction.

Put this on your watchlist and consider buying it on the spur of the moment.

UiPath

Robotic process automation (RPA) allows software to mimic human behavior and automate tedious tasks. Consider a large company where employees need to download documents, fill out forms, and enter information into accounting systems. Automating this process has a significant impact on enterprise efficiency. This is why I own shares in his RPA provider, UiPath (PATH).

UiPath ended fiscal 2024 with sales of $1.3 billion and annual recurring revenue (ARR) of $1.5 billion (growth of 24% and 22%, respectively). The company has a strong balance sheet with $1.9 billion in cash and investments and no long-term debt. We have a growing presence among large customers, with a total customer base of over 10,800.

FY25 guidance is weak at just 18% ARR growth, but this gives management an opportunity to beat this. It also means that UiPath's sales are worth a reasonable 9.5x his. Businesses are focused on how AI can increase efficiency and profitability, and this presents a great opportunity for UiPath to showcase its solutions.

Palantir

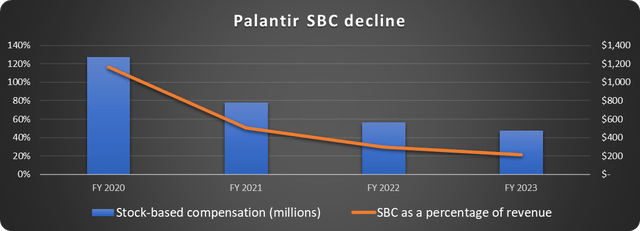

For years, Palantir's (PLTR) challenges have been excessive stock-based compensation (SBC) and unprofitability, and rightfully so. However, the company has just achieved his fifth straight profitable quarter, and his SBC has declined sharply, as shown below.

Data source: Palantir. Graph by author.

While the company has a strong presence in the defense industry, its treasure trove is the U.S. commercial market. Competition is fiercer than ever, and many companies will look to Palantir for data analytics and AI assistance.

U.S. commercial sales increased 70% year-over-year to $131 million in the fourth quarter, with total customer numbers increasing 35%. Palantir is holding a “bootcamp” to introduce potential customers to the new AIP platform, which has a big impact on sales. It's one thing to see a demo, but it's much better to immediately show your customers how to apply it directly to their business.

Palantir's solid balance sheet reports $3.7 billion in cash and investments and no long-term debt. It's no coincidence that Arm, UiPath, and Palantir have strong financial foundations and are on this list.

marvel technology

The ultimate deal with AI is to invest in companies that make the parts that move and store data. Marvell Technology (MRVL) meets this requirement with processors, controllers, switches, and other products for data centers, consumer electronics, automotive, and other industries. AI and custom computing are big growth opportunities for Marvell as huge data centers are built.

Marvell's revenue doubled in just two fiscal years from $2.9 billion to $5.9 billion, but growth took a breather in fiscal 2024, when revenue declined 7% to $5.5 billion. The company issued a lukewarm outlook for the first quarter of 2025 given weak consumer, carrier and networking demand, but expects data center revenue to increase. With the economy doing better than most expected, Marvell has a big chance to beat expectations.

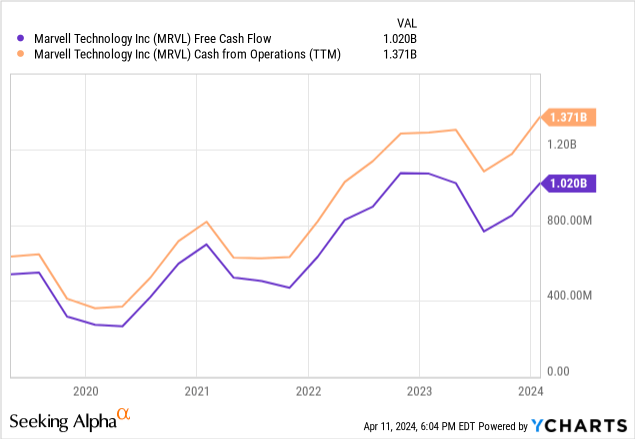

Although Marvell is not yet profitable on a GAAP basis, many of its expenses are non-cash items such as depreciation and amortization of intangible assets. For this reason, I focus on free cash flow growth, which has been steadily increasing, as shown below.

Management has work to do to resume overall revenue growth, but the long-term opportunity is significant.

Will an AI bubble occur?

As always, be wary of speculative companies. Proper position sizing and diversification is key. Some stocks I won't touch on right now due to valuation, but others are best suited for long-term investing.

A bubble occurred in July 1999, but the Nasdaq rose another 86% before reaching its peak. So, assuming there is a bubble, the correct question is: How many times is it now?