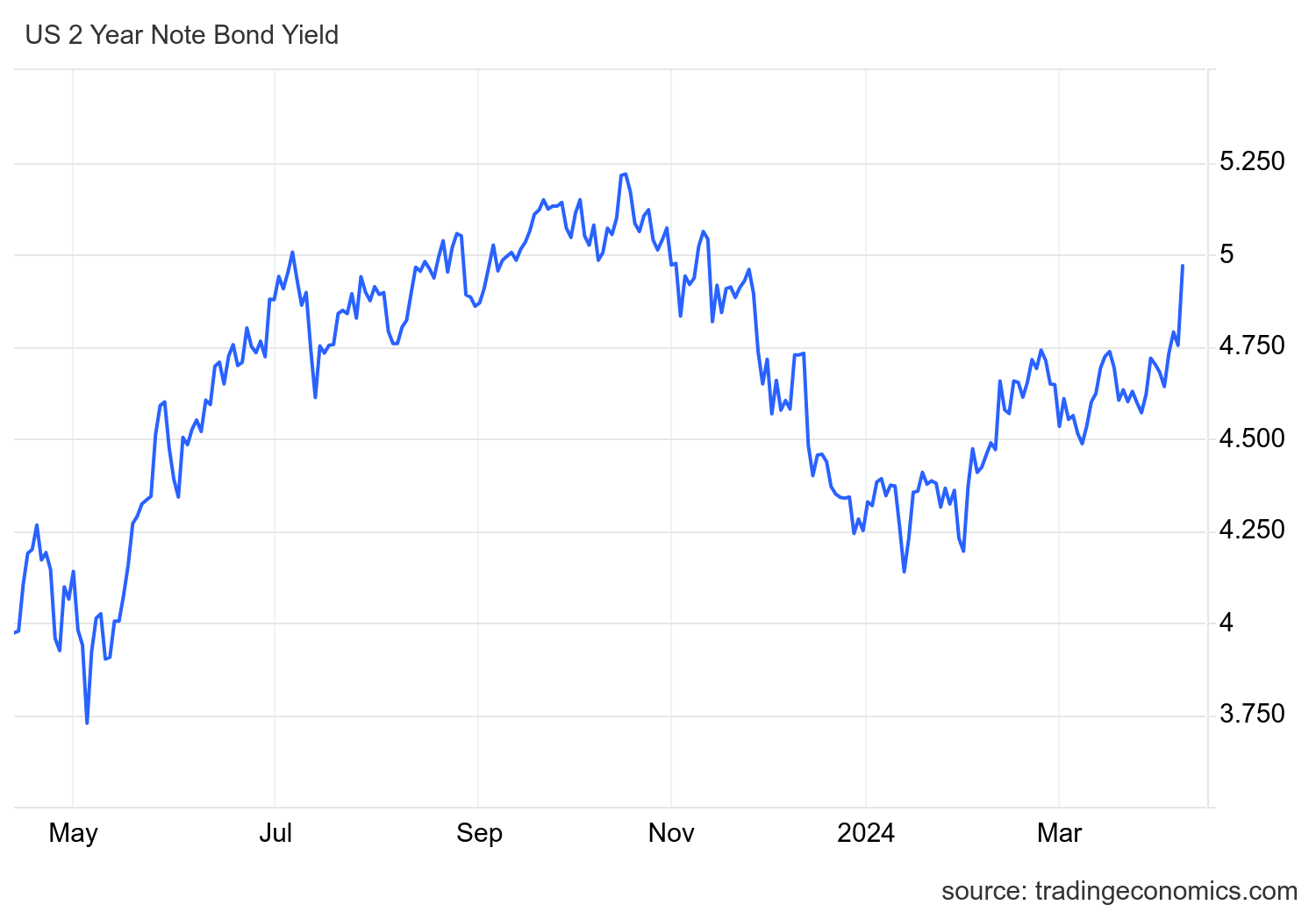

Until now, we have maintained a market line that has priced in three rate cuts, but today marks a clear break from that. At the beginning of this year, the market was ahead of the curve by saying there would be six rate cuts, but like last year, I believe the bond market was too bearish about the economy to price in six rate cuts. There's still plenty of time in 2024, but as you can see in the chart below, two-year bond yields have been on a roller coaster since last November.

from BLS: The U.S. Bureau of Labor Statistics announced today that the Consumer Price Index for all cities (CPI-U) rose a seasonally adjusted 0.4% in March, the same rate of increase as in February. Over the past 12 months, the all-item index rose 3.5% before seasonal adjustment.

Note: This report does not 100% reflect shelter inflation, which was higher than estimated. Car insurance and energy prices have also increased recently. However, the giant monster in the world of CPI is a haven, as it accounts for his 44.4% of the index.

Shelter inflation

The report states that shelter inflation had a negative impact on monthly inflation growth as owner-occupied housing equivalent rent (OER) is the main driver of monthly inflation.

Regarding shelter inflation, as you can see below, slow-moving monsters just aren't dropping fast enough to bring down core inflation data. In terms of CPI inflation, rents are the biggest contributor to core inflation. If month-on-month inflation rises, year-on-year data will slow down enough to sustain CPI gains.

rental data

OER has become a more important issue for CPI data this year. It should also be noted that while there is disinflation in apartments, rents for single-family homes have remained steady. However, this index slowdown causes the data to remain elevated. A more real-time shelter model would quickly change the story, but that's not happening.

Core CPI

We've made some progress on core CPI, but keep in mind. The Fed is not tracking CPI inflation toward its 2% target. That's PCE inflation, and the difference between CPI and PCE inflation is huge. Historically, we see a gap of 0.47%. Now it's double that. However, as shelter inflation has been declining slowly over the years, core CPI has stalled to the point where this data line is well below it.

Mortgage rates rose today as the Fed decided to cut interest rates by 1 as CPI forecasts missed by 0.1%. I don't believe the Fed will change course until the labor market collapses, which I talked about on this HousingWire Daily podcast. There are some trends in wage growth that would make the Fed more dovish, but the labor data won't break down until jobless claims rise.

We then get the PPI inflation data which is filtered down to the all-important PCE inflation data. stay tuned!