This week, the Office of the Comptroller of the Currency (OCC) Asked Thank you to America's financial institutions (FIs) for helping them “improve the financial capabilities and financial health of their customers.”

In a statement released Tuesday (April 2), the OCC said the best way for financial institutions to accomplish this is by reaching out to consumers, especially those who are currently “underserved” by the industry. He said he believes in providing “high-quality financial literacy education.”

The request was issued to coincide with the start of National Fiscal Capacity Month, which begins in April. But as PYMNTS Intelligence data shows, consumers seek trusted financial advice from financial institutions year-round.

Actually, “seeking advice” is an understatement. According to PYMNTS Intelligence, “How CU can help young consumers experiencing financial hardship” 59% of FI customers expect their financial institution to help them improve their financial health.

This report was completed with the help of: P.S.C.U., found that the need for financial advice is particularly acute among young consumers. His 29% of Gen Z consumers surveyed admitted they didn't know their credit score. This may not be surprising given that 79% of Gen Z and Millennials say they get financial advice through social media. Only 11% said they use a financial advisor to get the direction they need.

Another PYMNTS intelligence tracker, “Building financial assets through personalization beyond traditional banking” found a similar pattern in the UK.

Tracker has found that a growing number of young people in the UK are turning to TikTok influencers for budgeting and personal financial advice. 58% of his Gen Z consumers in the UK say they follow 'finfluencers' on TikTok, and of those, 26% of them follow more than the professional financial providers they consult. We also believe that social media gurus can provide better advice.

46% of UK-based Gen Z respondents said TikTok influencers were helpful when it came to providing topic-specific advice such as saving money, investing, and even choosing a mortgage. One in three people say they’ve even been alerted to an offer by an influencer. That led them to consider switching her FI.

“Personalization beyond traditional banking to build financial assets”” was born in collaboration with. NCRwe also identified financial education resources that U.S. consumers are seeking.

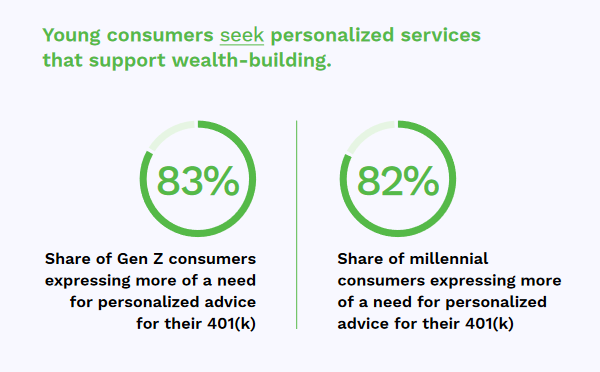

Their wish list includes tools to help them save for retirement, build an emergency savings account, and better manage their debt. Consumers in the United States especially wanted personalized advice on financing and managing their 401(k) accounts. 83% of Gen Z respondents and 82% of Millennials said they would appreciate such guidance, as did 79% of Gen X respondents and 67% of Baby Boomers.

National Financial Competency Month is a perfect opportunity for financial institutions to meet the OCC's call by helping their customers expand their financial education. But as the findings of his two PYMNTS Intelligence reports mentioned in this article make clear, consumers, especially younger consumers, are more likely to believe in authoritative and trustworthy information about credit scores, budgeting, saving, investing, and more. Sounds like you're seriously in need of any advice you can get.

Addressing this need could serve as a type of public service, and given that the OCC is a government agency, this concern is understandable. Perhaps more importantly for financial institutions, offering this type of financial literacy education is a valuable opportunity to deepen relationships with existing customers while attracting new customers seeking guidance.

Failure to do so represents a missed opportunity not only for financial institutions but also for consumers, who are likely to turn to self-proclaimed financial “experts” flocking to social media platforms.