meanwhile Nvidia's (NASDAQ:NVDA) The AI-fueled stock rally may not be over yet, and as GPU makers' valuations soar, it's becoming increasingly difficult to justify buying the stock. The stock, which had a market capitalization of $2.2 trillion as of midday Wednesday, is asking investors to ignore the myriad threats that could shake the company's dominance in the AI chip market. There is.

Nvidia's biggest advantage is in its software. CUDA is Nvidia's software toolkit for developing applications that can be accelerated by GPUs. CUDA has been around for 16 years and has become the de facto standard. As the AI boom began, the path of least resistance was his Nvidia GPU and his CUDA-powered software.

Although there are alternatives to CUDA, there is a great deal of inertia in maintaining Nvidia's lead.Without this software advantage, competing AI chips AMD, intelother companies will find it easier to gain market share.

Nvidia recently updated its CUDA end-user license agreement to explicitly prohibit transformation layers that allow CUDA-based software to run on non-Nvidia hardware. The company is clearly concerned that competition will undermine its dominant market position. The end of CUDA's dominance will be a boon for any company purchasing an AI accelerator, and it's likely to happen sooner rather than later as AI companies explore alternatives.

A low-risk way to bet on AI

Although Nvidia's competitive advantage may erode over time as competition increases; international office machine (NYSE:IBM) has established itself as the go-to AI platform among large enterprises and organizations. The company's watsonx AI platform. Its name comes from his award-winning Watson AI supercomputer. danger! Launched in 2011, the service is aimed at the type of customers who can't let their guard down when it comes to adopting AI technology.

The watsonx platform allows enterprises to train, validate, and deploy AI models while being mindful of compliance, risk management, and governance issues. Companies operating in highly regulated industries must follow strict rules regarding data, and no company wants their customer-facing AI chatbots to go off the rails. IBM's watsonx platform provides guardrails for companies implementing AI.

Beyond common use cases, watsonx has some specific features that can accelerate adoption. IBM's mainframe systems have been at the heart of some industries for decades, running billions of lines of sensitive, mission-critical code written in an ancient programming language called COBOL. IBM's mainframe customers are feeling the pinch as the number of developers who can write and maintain COBOL code dwindles.

This is where watsonx Code Assistant comes into play. One of the applications of this product is to modernize COBOL code by converting it to Java code. Much of this code is highly sensitive, so this process must be done carefully. Consider the software that processes transactions at a major financial institution. This feature not only encourages customers to adopt his Watsonx platform, but also strengthens the mainframe business by making it much easier to modernize applications.

Still in stock at bargain prices

IBM's stock price has risen over the past year, rising about 50% during that time. The company's optimism about his AI prospects and a series of solid results are likely behind this surge.

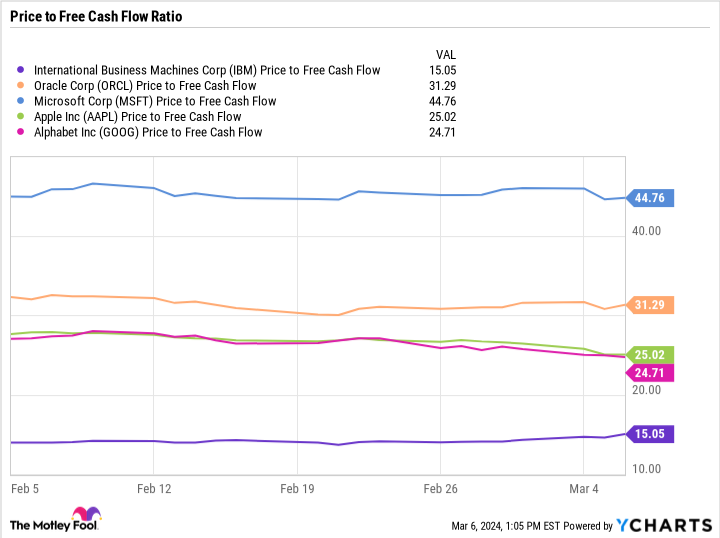

Even as IBM stock nears all-time highs, the stock remains a great value for investors. The company expects to generate about $12 billion in free cash flow this year, giving it a price-to-free cash flow ratio of 15x. For comparison, other large tech companies trade at significantly higher multiples of free cash flow.

Although AI is just one part of IBM's business, it could be a major growth driver in the coming years. The stock isn't as cheap as it once was, but it's still an attractive investment for those looking to take advantage of the AI boom without taking on too much risk.

Should you invest $1,000 in International Business Machines right now?

Before buying International Business Machines stock, consider the following:

of Motley Fool Stock Advisor Our analyst team has identified what they believe Best 10 stocks What investors should buy right now…and International Business Machines was not among them. These 10 stocks have the potential to generate impressive returns over the next few years.

stock advisor provides investors with an easy-to-understand blueprint for success, including guidance on portfolio construction, regular updates from analysts, and two new stocks each month.of stock advisor Since 2002, the service has more than tripled S&P 500 returns*.

See 10 stocks

*Stock Advisor returns as of March 8, 2024

Alphabet executive Suzanne Frye is a member of The Motley Fool's board of directors. Timothy Green holds a position with International Business Machines. The Motley Fool has positions in and recommends Alphabet, Apple, Microsoft, Nvidia, and Oracle. The Motley Fool recommends International Business Machines and recommends the following options: A long January 2026 $395 call on Microsoft and a short January 2026 $405 call on Microsoft. The Motley Fool has a disclosure policy.

Missed Nvidia? This enterprise AI stock remains a bargain.Originally published by The Motley Fool