If you have any questions, please contact us. Nvidia's (NASDAQ:NVDA) The stock market's ability to maintain its frenetic momentum came to an end last week following the release of the company's fiscal 2024 fourth-quarter results (quarter ending January 28). The semiconductor giant not only shattered Wall Street's expectations, but also provided strong guidance for the quarter, suggesting that growth fueled by artificial intelligence (AI) will continue.

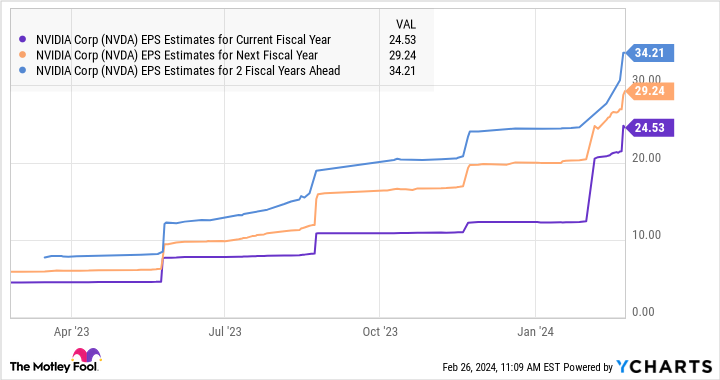

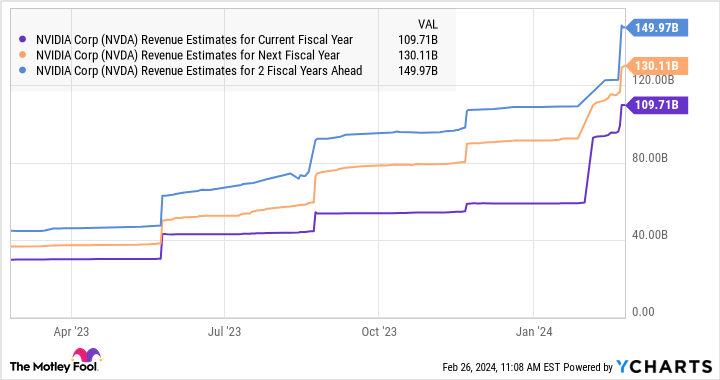

Unsurprisingly, Nvidia stock soared impressively after the earnings release. Moreover, analysts have started raising their growth forecasts for the current fiscal year and the next two fiscal years, suggesting that its outstanding growth will continue.

However, a key statement from Nvidia CFO Colette Kress on NVIDIA's earnings call suggested that the company could sustain its impressive growth for even longer, stating that “approximately 40% of data center revenue over the past year We estimate that % is due to AI inference.”

Let's take a look at the details.

AI inference could help Nvidia maintain its lead in this lucrative market

Nvidia's graphics processing units (GPUs) have been in the spotlight since they were revealed to play a mission-critical role in training the large-scale language models (LLMs) that form the backbone of popular generative AI applications such as ChatGPT. I took a bath. Multiple cloud service providers are lining up to get their hands on Nvidia's GPUs to train AI models and bring generative AI services to market. As a result, Nvidia controls a whopping 90% share of the AI training chip market.

After all, demand for Nvidia's flagship H100 AI GPU is so strong that customers are willing to wait between 36 and 52 weeks to get their hands on this hardware. Nvidia is ramping up its supply capacity to meet its robust demand, and this is likely to help the company continue to grow at a breakneck pace, with sales expected to reach $60.9 billion by fiscal year 2027 compared to his $60.9 billion in fiscal year 2024. It explains why it is expected to reach more than twice his number.

But Kress' comments that 40% of Nvidia's data center revenue comes from selling chips used in AI inference applications suggests that Nvidia could sustain its impressive growth over the long term. . This is because AI inference chips are expected to account for the majority of the overall AI chip market. According to TechSpot, a provider of technology news and analysis, the inference is that he is expected to account for 45% of the AI chip market, and that in the future he will have AI training that his chips will account for his 15% of this area. It will be like this.

This is not surprising. That's because when you train an AI model using general-purpose computing chips, such as graphics cards sold by Nvidia, that model is used to generate results using new data sets. This process of generating results from an already trained AI model is known as inference. Verified Market Research estimates that by 2030, demand for AI inference chips could surge from his estimate of $16 billion in 2023 to nearly $91 billion in 2030.

According to Kress' statement, Nvidia sold $19 billion worth of AI inference chips last year (40% of its total data center revenue of $47.5 billion that year). This exceeds Verified Market Research's estimated sales of $16 billion. This means that Nvidia already dominates his AI inference market and the potential revenue opportunities bode well for the company's future.

If the AI inference chip market does indeed generate $90 billion in revenue, as estimated by Verified Market Research, Nvidia's data center revenue could continue to grow steadily through the end of the decade, significantly boosting its overall business. .

Additionally, Nvidia is taking steps to remain a leading player in the AI inference space, with an eye toward a potential transition to custom chips, formally known as application-specific integrated circuits (ASICs). These chips are specifically designed for AI inference purposes due to their computing power and low power consumption. According to third-party estimates, the market for custom chips used in inference could surge from an estimated $30 billion in 2023 to $50 billion in 2025.

Overall, it's easy to see why analysts are predicting impressive growth for Nvidia.

Valuation makes the stock an attractive buy

Nvidia's revenue and revenue are set to grow rapidly over the next few years. If he can actually deliver on that front, the market should ideally see him deliver a sizable return on Nvidia stock.

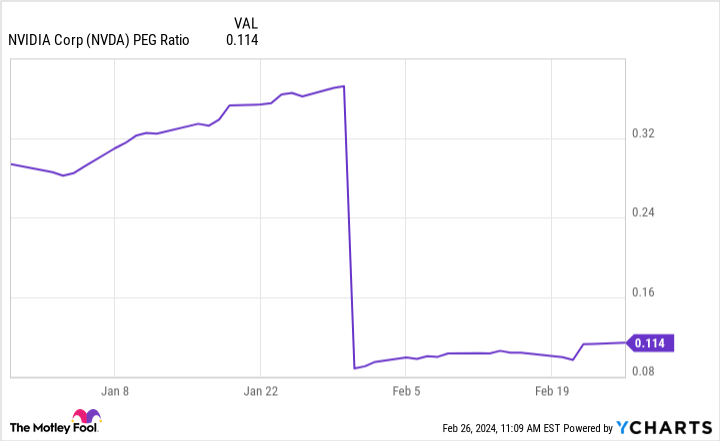

That's why this AI stock seems like a no-brainer to buy now, especially considering the company's forward earnings multiple of 33 is currently lower than its five-year average forward earnings multiple of 39. On the other hand, NVIDIA's price remains very low. /Earnings to Growth (PEG Ratio).

The PEG ratio is calculated by dividing a company's P/E ratio by the estimated annual earnings growth rate that the company can achieve. As the following chart shows, NVIDIA's PEG ratio is well below 1. Below this value, the stock is considered undervalued.

All of this means that despite last year's huge surge, investors are still well-earned in Nvidia, and the company is doing well to ensure solid growth. The move means you should consider buying this AI stock directly.

Should you invest $1,000 in Nvidia right now?

Before buying Nvidia stock, consider the following:

of Motley Fool Stock Advisor Our analyst team has identified what they believe Best 10 stocks What investors can buy right now…and Nvidia wasn't among them. These 10 stocks have the potential to generate impressive returns over the next few years.

stock advisor provides investors with an easy-to-understand blueprint for success, including guidance on portfolio construction, regular updates from analysts, and two new stocks each month.of stock advisor Since 2002, the service has more than tripled S&P 500 returns*.

See 10 stocks

*Stock Advisor will return as of February 26, 2024

Harsh Chauhan has no position in any stocks mentioned. The Motley Fool has a position in and recommends Nvidia. The Motley Fool has a disclosure policy.

“90 Billion Easy Reasons to Buy Nvidia Stock Now'' was originally published by The Motley Fool.