stocks in 3 years Nvidia")

Over the past 30 years, no next big trend or innovation has matched the advent of the Internet. But artificial intelligence (AI) has the potential to do for this generation of businesses what the internet did for American businesses 30 years ago.

PwC analysts predict that by the turn of the decade, AI, which relies on software and systems to replace human oversight, will add $15.7 trillion to global gross domestic product.No company has benefited more directly from the AI revolution than semiconductor stocks. Nvidia (NASDAQ:NVDA).

Nvidia stock may be in a bubble

In 15 months, Nvidia's valuation rose $1.9 trillion to $2.26 trillion, making it the second-highest valuation. microsoft and apple Among US listed companies

Nvidia's superior performance reflects the overwhelming demand for its high-performance A100 and H100 graphics processing units (GPUs). Some analysts believe NVIDIA's top-of-the-line chips could account for more than 90% of the GPUs deployed in AI-powered data centers this year. The early scarcity associated with these chips gave Nvidia extraordinary pricing power.

But there are also many reasons to believe that NVIDIA is in a bubble.

For example, every next big trend or innovation of the past 30 years has gone through an initial bubble. Investors have a tendency to overvalue the introduction of new technologies, and I expect AI to be no exception.

NVIDIA may also see less pricing power in the coming quarters as new competitors enter the space and in-house production reduces the scarcity of AI-GPUs. A large portion of Nvidia's 217% data center sales growth in fiscal year 2024 (ending January 28, 2024) is due to its pricing power.

The biggest concern may be that the top four customers in the Magnificent Seven, which account for about 40% of sales, are all developing their own AI chips for data centers. In any case, orders from NVIDIA's top customers are likely to taper off in the coming quarters.

If history rhymes once again and the AI bubble bursts, Nvidia's market cap could plummet (in relation to the current situation), allowing other companies to jump on it.

Here are five companies, excluding Microsoft and Apple, that have already outperformed Nvidia. These companies have the tools and intangibles that in three years he will be worth more than Nvidia.

1. Alphabet: Current market cap $1.88 trillion (Class A shares, GOOGL)

Here's the first industry giant that could comfortably surpass Nvidia's market cap over the next three years. alphabet (NASDAQ:Google)(NASDAQ:GOOG)the parent company of internet search engine Google, streaming platform YouTube, self-driving car company Waymo and others.

The reason Alphabet will hold up much better than Nvidia if the AI bubble bursts is because Alphabet is a bona fide monopoly in internet search. In March, Google accounted for more than 91% of the world's Internet search share. Looking back at his nine years of monthly data from GlobalStats, Google hasn't ceded more than his 10% of the world's internet search share to any other company. Combined. For advertisers looking to get their message in front of users, this is the obvious choice and will benefit greatly from long-term domestic and international growth.

Google Cloud could thrive even as Nvidia stumbles. Enterprise cloud spending is still in its infancy, and as of September 2023, Google Cloud accounts for 10% of the global cloud infrastructure services share. Cloud profits have traditionally been richer than advertising profits, so Alphabet's cash flow growth could accelerate going forward. Late 10's.

2. Amazon: Current market capitalization is $1.87 trillion

E-commerce giants like Alphabet Amazon (NASDAQ:AMZN) If the AI bubble deflates, it could be back ahead of Nvidia at some point over the next three years.

Most people are familiar with Amazon, the world's leading online marketplace. In 2023, an estimated 38% of online retail spending in the US will be traced to e-commerce sites. But the real benefit of having more than 2 billion people visit his website on Amazon every month is the advertising revenue Amazon generates and the subscription revenue that comes in through Prime. Amazon surpassed 200 million Prime users in April 2021, and has almost certainly increased this number since becoming Amazon's exclusive streaming partner. thursday night football.

But Amazon's main cash flow driver is its cloud infrastructure services platform. Amazon Web Services (AWS) consistently generates between 50% and 100% of Amazon's operating profit, even though it accounts for one-sixth of the company's net sales. According to Canalys, AWS is the world's number one cloud infrastructure services platform by spend.

3. Metaplatform: Current market capitalization is $1.24 trillion

It's a social media company meta platform (NASDAQ:Meta) is betting on a future powered by AI and augmented/virtual reality, which should help its core business sustain double-digit profit growth and boost its valuation well beyond Nvidia by 2027 .

Meta's “secret sauce” isn't a secret at all. Despite his metaverse ambitions and big spending on Reality Labs, the company's bread and butter continues to be social and his media empire. The company is the parent company of the most visited social site on the planet (Facebook), and its family of apps combined had just under 4 billion monthly active users in the December-end quarter. Just as advertisers are willing to pay a premium for Alphabet Inc.'s Google because of its dominance in Internet search, Meta's ad pricing power tends to be superior in most economic conditions.

Another reason Meta shines and could completely close its roughly $1 trillion valuation gap with Nvidia over the next three years is its balance sheet. Meta is a cash flow machine. Operating income last year exceeded $71 billion, and the company ended 2023 with $65.4 billion in cash, cash equivalents and securities. This cash not only cushions the company against downside prices, but also gives Meta the luxury of seizing opportunities that few other companies can match.

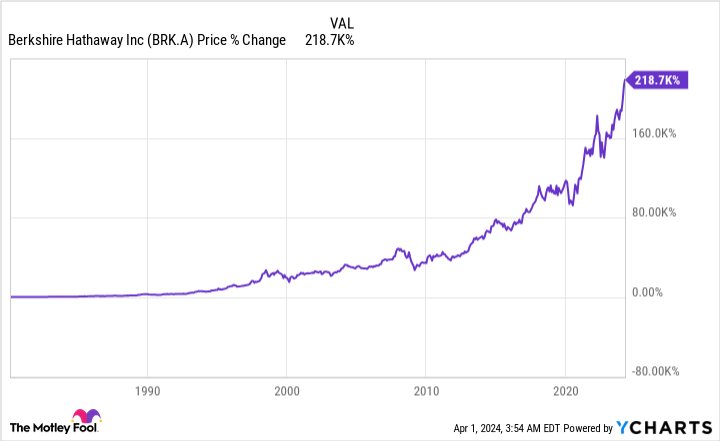

4. Berkshire Hathaway: Current market cap of $908 billion (Class A shares, BRK.A)

The fourth company that could surpass AI stock Nvidia's market capitalization in the next three years is a conglomerate. berkshire hathaway (NYSE: BRK.A)(NYSE: BRK.B). Since Warren Buffett took the helm at Berkshire Hathaway in the mid-1960s, the company's Class A shares have averaged an annual return of nearly 20%.

One of the main reasons Berkshire Hathaway is so lucrative for investors is the Oracle of Omaha's love of dividend stocks. Berkshire plans to collect about $6 billion in dividends this year, with its five core holdings alone accounting for about $4.4 billion in total dividend income. Dividend-paying companies are recurringly profitable and often have a proven track record, making them exactly the type of companies expected to grow in tandem with the U.S. economy over the long term.

Warren Buffett and his investment team are also attracted to branded companies with trusted management teams. For example, his $155 billion investment in Apple amounts to nearly 42% of Berkshire Hathaway's invested assets. Apple is one of the world's most valuable brands, and CEO Tim Cook has done a remarkable job leading continued physical product innovation while also pivoting the company toward a subscription-services-driven future. I've been working.

5. Visa: Current market cap is $573 billion

The fifth stock that will be worth more than artificial intelligence stock Nvidia in three years is a payment processing giant. visa (NYSE:V). As it stands, Visa needs to close a valuation gap of nearly $1.7 trillion. But that could happen if the AI bubble bursts and Visa continues to do what it has been doing for decades.

What drives Visa is that the company has a long opportunity. The company is the undisputed market share leader in credit card network purchasing volume in the United States (the world's largest consumer market) and is expanding its payments infrastructure organically and in underbanked regions such as the Middle East, Africa, and Africa. We have a multi-decade opportunity to pursue acquisitionally. Southeast Asia. Visa should be able to maintain double-digit earnings growth through the rest of the decade, if not much longer.

Another source of Visa's success is its relatively conservative management team. Although the company will likely be a huge success as a lender, its leaders have chosen to keep the company focused solely on payment facilitation. The advantage of this approach is that since Visa is not a lender, it does not need to set aside capital to cover loan losses during economic downturns. As a result, profit margins always remain above 50%.

Should you invest $1,000 in Nvidia right now?

Before buying Nvidia stock, consider the following:

of Motley Fool Stock Advisor Our analyst team has identified what they believe Best 10 stocks What investors can buy right now…and Nvidia wasn't among them. These 10 stocks have the potential to generate impressive returns over the next few years.

stock advisor We provide investors with an easy-to-understand blueprint for success, including guidance on portfolio construction, regular updates from analysts, and two new stocks every month.of stock advisor Since 2002, the service has more than tripled S&P 500 returns*.

See 10 stocks

*Stock Advisor will return as of April 1, 2024

John Mackey, former CEO of Amazon subsidiary Whole Foods Market, is a member of the Motley Fool's board of directors. Randi Zuckerberg is a former head of market development and spokesperson at Facebook, sister of Meta Platforms CEO Mark Zuckerberg, and a member of the Motley Fool's board of directors. Alphabet executive Suzanne Frye is a member of The Motley Fool's board of directors. Sean Williams has held positions at Alphabet, Amazon, Meta Platforms, and Visa. The Motley Fool has positions in and recommends Alphabet, Amazon, Apple, Berkshire Hathaway, Meta Platforms, Microsoft, Nvidia, and Visa. The Motley Fool recommends the following options: A long January 2026 $395 call on Microsoft and a short January 2026 $405 call on Microsoft. The Motley Fool has a disclosure policy.

Prediction: 5 stocks that will be worth more than artificial intelligence (AI) stocks in 3 years Nvidia Originally published by The Motley Fool.